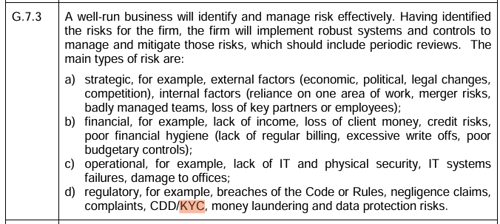

UK/Jersey family solicitors [or any other lawyer] are they caught as TAX ADVISORS and therefore the AML rules?

04/07/2025

In the UK, family solicitors are not directly regulated under the Money Laundering Regulations (‘the Regulations’) or in Jersey under SCH2 of the Proceeds of Crime (Jersey) Law 1999 and the underlying Money Laundering (Jersey) Order 2008 (MLJO)

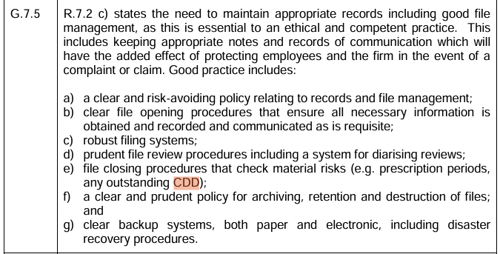

CDD - SRA AND JERSEY RULES FOR LAWYERS

Both the SAR and the Jersey law society expect firms to do some CDD

- The SRA have always included a requirement for all solicitors, regardless of the sector, to check the identity of their client (paragraph 8.1 of the Code of Conduct for Individuals),

However, the Law Society of Jersey Code of Conduct do not expressly require CDD unless there is a regulatory compulsion.

ARE SOME LAWYERS TAX ADVISERS

Justine Cadbury, a Professional Support Lawyer at Stowe Family Law LLP, highlighted the following issue in a recent article.

- Following the implementation of the 5th European Directive in January 2020, the status of family solicitors and the extent to which they must comply with the Regulations has become less clear.

- This is due to a subtle change of the definition of a ‘tax adviser’ under regulation 11(d) which has been expanded to include those who provide “material aid, or assistance or advice, in connection with the tax affairs of other persons, whether provided directly or through a third party, when providing such services”.

THE UK CHANGE

- The Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017, commonly referred to as the Money Laundering Regulations, set out the requirements for businesses to prevent money laundering and terrorist financing.

- These regulations apply to various sectors, including financial institutions, legal professionals, and tax advisers.

- Changes to the Definition of 'Tax Adviser' under Regulation 11(d)

- As of January 10, 2020, the definition of a 'tax adviser' under Regulation 11(d) of the Money Laundering Regulations was expanded. The updated definition now includes:

- Any firm or sole practitioner who, by way of business, provides

- Material aid, assistance, or advice in connection with the tax affairs of other persons.

- This definition covers services provided directly or through a third party .

- Any firm or sole practitioner who, by way of business, provides

- Implications of the Expanded Definition

- Broader Scope: The definition now encompasses a wider range of activities, including not just direct tax advice but also assistance and material aid related to tax matters .

- Increased Compliance Requirements: More professionals and firms are now required to comply with AML regulations, including customer due diligence, ongoing monitoring, and reporting suspicious activities .

- Enhanced Supervision: The expanded definition means that more businesses fall under the supervision of regulatory bodies, ensuring they adhere to AML/CTF requirements .

- This change aims to close loopholes and ensure that all entities involved in tax-related services are vigilant against money laundering and terrorist financing activities. If you need more detailed information or have specific questions, feel free to ask!

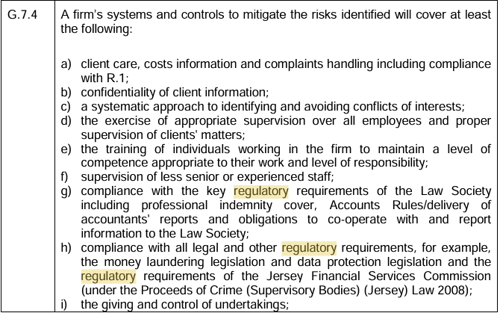

THE SRA

- The SRA has explained how it interprets this definition and that it’s likely to include situations where we refer a client to the HMRC website for something specific. As the breakdown of a relationship can have tax implications, it’s likely to also include circumstances where we refer a client to an accountant to obtain a forensic report or for advice on capital gains tax liabilities.

- In line with the interpretations being applied by the SRA, it’s highly likely that we will fall within the definition of a tax adviser and consequently, under the scope of the Regulations. In light of this, their expectation is that we’ll be 100% compliant on all cases.

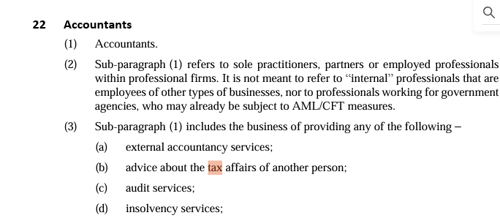

IN JERSEY

Under 22 of SCH2 of the POCL if a lawyer [firm] is in the business of providing advice about the tax affairs of another person, they are caught as “accountants [!!] and therefore required to apply the standards of the MLJO.

https://www.jerseylaw.je/laws/current/PDFs/L_8_1999.pdf

SOURCES

- https://careers.stowefamilylaw.co.uk/blog/2022/09/08/family-lawyers-what-are-your-money-laundering-obligations/#menu

- https://www.jerseylawsociety.je/society/code-conduct /

- https://www.jerseylawsociety.je/application/files/1216/9055/9942/THE_LAW_SOCIETY_OF_JERSEY_CODE_OF_CONDUCT-_1_JANUARY_2017.pdf

- Guidance for tax advisers in the scope of the AML regulations

- Money laundering and terrorist financing (amendment) regulations 2019

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.