The JFSC guide on Article 36 of the Proceeds of Crime (Jersey) Law 1999 is being reviewed – have your say.

02/09/2025

The JFSC are reviewing the guidelines on the interpretation of Article 36 of the Proceeds of Crime (Jersey) Law 1999 as part of its Schedule 2 refresh project.

The JFSC

- Want to make sure the updated guidelines are practical, easy to understand, and work for all types of financial services businesses.

- Want you to share your feedback to help shape and improve the guidelines at one of their drop-in sessions.

Drop-in sessions

- Monday 29 September 2025 – 09:00 am – 12:00 pm: https://lnkd.in/eZFrFn2i

- Friday 3 October 2025 – 10:00 am – 13:00: https://lnkd.in/eR3dM6xb

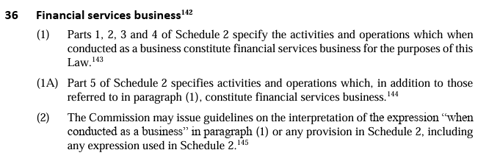

The official guidance on Article 36 of the Proceeds of Crime (Jersey) Law 1999, issued by the Jersey Financial Services Commission (JFSC).

- This guidance helps interpret the law, especially the phrase “when conducted as a business” and the scope of Schedule 2 activities.

🔍 Key Points from the Guidance

1. Purpose of the Guidelines

- Issued under Article 36(2), allowing the JFSC to clarify what constitutes financial services business.

- Helps determine whether an activity falls within the scope of Schedule 2 and whether it's conducted as a business.

2. Two-Part Test for Scope

To determine if a person is carrying on a financial services business:

- Part 1: Are the activities listed in Schedule 2?

- Part 2: Are those activities conducted as a business?

3. Interpretation of “Conducted as a Business”

- This is not always clear-cut and may require subjective judgment.

- The JFSC refers to FATF Standards for guidance, which are not prescriptive but provide a framework.

- Activities like banking are inherently business-like, while others (e.g., lending money informally) may not be.

4. Registration Requirements

- If both criteria are met, the person must register with the JFSC as a Schedule 2 business.

- Non-Professional Trustees are an exception—they are considered financial services businesses but do not need to register.

5. Consequences of Non-Compliance

- Operating without registration may breach Article 10 of the Supervisory Bodies Law, carrying penalties of up to 7 years imprisonment and/or a fine.

Access the Full Guidelines

- You can read the full document here: 👉 JFSC Guidelines on Interpretation of Article 36 (PDF)

- https://www.jerseyfsc.org/media/7787/guidelines-on-interpretation-reformatted-30-sept-24.pdf

Sources

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.