New Criminal Offence for 'Reckless Untruth' in Direct Tax Declarations [HMRC Launches Consultation]

26/06/2026

23 June 2026 – Consultation closes 16 August 2026

- HMRC has opened a public consultation on introducing a new criminal offence for making reckless, untrue statements or declarations in direct tax matters.

- The proposal would align direct tax with existing rules that already apply to indirect taxes (VAT and customs).

- The government says the aim is to ensure consistency across tax regimes and to ensure that those who engage in "highly culpable serious non-compliance" can be "fairly tried and properly brought to justice".

Why HMRC says existing fraud laws are not enough

- Many people assume that serious reckless statements in tax returns would already be caught by the Fraud Act 2006 or the common law offence of cheating the public revenue.

- However, HMRC states that these existing offences generally require proof of dishonesty.

- In some cases, prosecutors struggle to prove dishonesty to the criminal standard — even where the behaviour is seriously reckless and has caused significant loss to the Exchequer.

- The new offence is specifically designed to fill this gap by allowing prosecution for recklessness alone, without needing to prove dishonesty.

How "recklessness" is defined in the proposal

- The consultation defines recklessness in line with existing criminal law principles:

- A person acts recklessly if they:

- Are aware of a risk that the statement or declaration is untrue, and

- In the circumstances known to them, it is unreasonable to proceed with making the statement despite that risk.

- This sits between:

- Carelessness (civil penalties only), and

- Dishonesty/deliberate conduct (prosecuted under existing higher-tariff fraud or evasion offences).

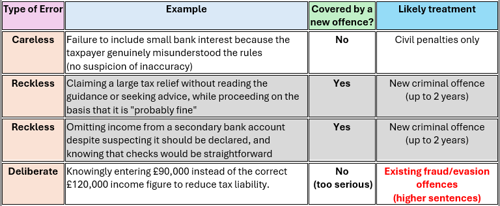

Specific examples from the consultation document

The consultation includes a helpful table distinguishing the different levels of behaviour:

These examples show that the new offence is aimed at cases where the person knew there was a real risk the statement was wrong but chose to carry on anyway, without necessarily having a dishonest intent to defraud.

Key details of the proposed offence

- It would apply to statements and declarations in direct tax matters (income tax, corporation tax, capital gains tax, etc.).

- It would be an "either way" offence (can be tried in magistrates' court or Crown Court).

- Maximum penalty: 2 years' imprisonment and/or an unlimited fine (aligned with the equivalent indirect tax offence under the Customs and Excise Management Act 1979).

- It would not replace existing fraud prosecutions — those would continue to be used where dishonesty can be proven.

What should taxpayers and advisers do?

- While the offence is still at the consultation stage, the direction of travel is clear.

- Taxpayers and agents should ensure robust processes are in place for reviewing tax positions, documenting judgements, and seeking advice in higher-risk areas.

Consultation details

- Opened: 23 June 2026

- Closes: 11:59 pm on 16 August 2026

Responses should be sent to:

Official sources

This proposal forms part of the wider Tax Update 2026 package.

Primary sources:

- Main consultation page: https://www.gov.uk/government/consultations/proposed-offence-for-reckless-untrue-statements-direct-taxes

- Full consultation document (includes examples and detailed definition of recklessness): https://www.gov.uk/government/consultations/proposed-offence-for-reckless-untrue-statements-direct-taxes/introducing-a-criminal-offence-for-making-reckless-untrue-statements-or-declarations-in-direct-tax--3

Related:

- Summary of Tax Update 2026: https://www.gov.uk/government/publications/summary-of-tax-update-2026-simplification-modernisation-and-fairness

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.