Lenders and borrowers in VAT arbitrage in lending money laundering [Jersey NRA red flag]

11/09/2023

Jersey’s NRA highlights the following.

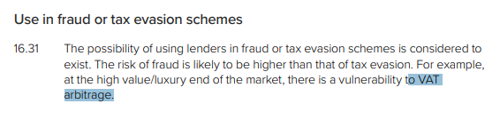

VAT arbitrage in lending money laundering is a scheme that involves exploiting the differences in VAT rates between countries or regions to obtain illicit profits.

For example,

- A lender may lend money to a borrower in a low-VAT jurisdiction and charge interest subject to VAT.

- The borrower may use the money to purchase goods or services in a high-VAT jurisdiction and claim a VAT refund.

- The lender and the borrower may share the difference between the VAT paid and the VAT refunded, thus laundering the money.

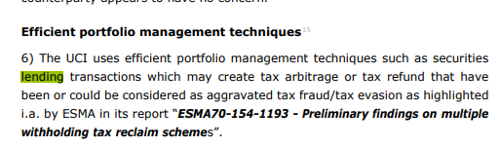

The Luxembourg CSSF regulator highlights this here.

This type of scheme may be detected by some indicators, such as:

- The use of shell companies or offshore entities to facilitate lending transactions.

- The lack of economic substance or business rationale for the lending transactions.

- The use of complex or unusual contractual arrangements that may create tax arbitrage or tax refund opportunities.

- The involvement of high-risk jurisdictions or sectors known for VAT fraud or evasion.

OTHER SOURCES RE TRADE-BASED ML

- https://www.oecd.org/tax/crime/money-laundering-and-terrorist-financing-awareness-handbook-for-tax-examiners-and-tax-auditors.pdf

- https://www.fatf-gafi.org/content/dam/fatf-gafi/reports/Trade-Based-Money-Laundering-Risk-Indicators.pdf

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.