JFSC says: Jersey TCSPs and FSBs demonstrate effective oversight and sound risk management

08/06/2026

On 3 June 2026, the Jersey Financial Services Commission (JFSC) published feedback from its 2025 prudential discovery visit programme.

- The JFSC visited 11 larger trust company businesses (TCB) and fund services businesses (FSB) (5 TCB-only and 6 dual-licensed) between November 2025 and February 2026.

- The visits were

- Not inspections or enforcement focused.

- Designed to help the JFSC understand how boards oversee financial resilience and the medium-term sustainability of non-bank business models in Jersey.

Overall finding: Positive.

- The firms demonstrated strong profitability, adequate liquidity, and effective governance practices that support sound risk management.

- The feedback paper sets out "what good looks like" from these more mature firms and identifies five key themes for all TCBs and FSBs to reflect on.

The message is constructive and proportionate:

- The sector is performing well, but boards should use these insights to strengthen arrangements, particularly around forward-looking analysis and information flow.

This is a helpful, well-timed piece of supervisory feedback.

- Firms that treat it as an opportunity for continuous improvement rather than another regulatory exercise will derive the most benefit

Key Themes for Reflection (with Good Practice Examples)

The JFSC grouped observations into five themes, each with examples of good practice observed during the visits:

- Liquidity management and adjusted net liquid assets (ANLA)

- Firms regularly assessed whether their ANLA processes remained aligned with JFSC guidance and reflected the current business model, asset mix, and risk profile.

- Liquidity levels were generally well above minimum requirements, with regular reporting to boards.

- Assurance and information flow to boards

- Boards received regular financial and management information.

- Firms used a combination of existing controls, review processes, and external audit.

- Some firms were considering how to obtain ongoing (not just point-in-time) assurance as activities and risks evolve.

- Governance and board oversight

- Boards had a strong mix of skills and experience.

- They demonstrated clear understanding of revenue drivers, costs, and key risks.

- Many boards held active discussions on financial performance and business model risks.

- Structures supported independent challenge, with clear arrangements to manage conflicts (especially where senior management also sit on the board).

- Concentration risk

- Most firms monitored reliance on a small number of clients or income streams and reported this to the board.

- Stronger firms considered the wider impact on financial resilience, liquidity, and long-term sustainability (e.g., what happens if a major client structure winds down).

- Financial resilience and forward-looking analysis

- Firms maintained stable, cash-generating business models. Some used proportionate horizon scanning, scenario analysis, and stress testing.

- A few considered group support or insurance as mitigations for unexpected adverse events.

- External factors (economic uncertainty, geopolitical developments) were increasingly being factored in.

Overall message from the JFSC:

- The 11 firms visited are profitable, liquid, and stable.

- They demonstrate sound financial management. These numbers are illustrative only; they come from larger, more mature firms and are not targets or benchmarks that every firm must hit.

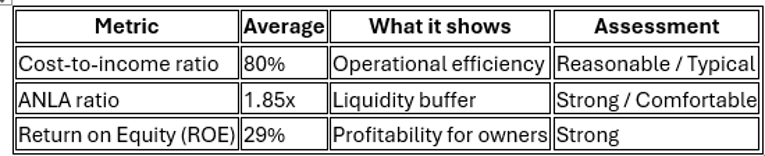

- Quantitative snapshot from the 11 firms (illustrative only):

- Average cost-to-income ratio: 80%

- Average ANLA ratio: 1.85x (well above requirements)

- Return on Equity: 29%

- See Appendix 1

- What does the Quantitative Snapshot mean?

Action List for Firms

- Boards and senior management should treat this as a self-assessment prompt, not a new compliance burden.

Immediate actions (next 4–6 weeks)

- Download and circulate the full feedback paper to the board and relevant committees.

- Schedule a dedicated board or risk committee discussion to review the five themes and assess relevance to your firm.

- Conduct a high-level gap analysis against the good practices described (document conclusions and any actions).

Short-term actions (by end Q3 2026)

- Review and enhance board Management Information (MI) to explicitly cover:

- ANLA trends/compliance,

- Concentration risk and impact analysis, and

- Forward-looking resilience indicators.

- Re-confirm that ANLA processes, calculations, and governance remain aligned with

- Current business activities and

- JFSC guidance.

- Assess board challenge arrangements, particularly independence and conflict management, where executives sit on the board.

Medium-term/ongoing actions

- Develop or refine proportionate forward-looking tools (scenario analysis/stress testing) focused on business model sustainability under adverse but plausible conditions (e.g., loss of key clients, cost shocks, market stress).

- Broaden concentration risk monitoring to include quantified impact assessments on liquidity, capital, and viability.

- Work with external auditors/advisors to explore how existing assurance work can better support internal resilience assessments without adding material cost.

- Monitor JFSC communications for upcoming workshops, updated ANLA guidance, or thematic discussions.

JFSC's Forward Agenda

The JFSC will:

- Embed these themes into day-to-day supervisory activity (proportionate to each firm's risk profile).

- Engage with industry bodies (e.g., Jersey Funds Association, Jersey Association of Trust Companies) for shared learning.

- Work with auditors and advisors on assurance enhancements.

- Offer targeted workshops where there is demand.

Our View: What Changes Firms Need to Undertake

The update isn't a warning of widespread problems; it's a benchmark exercise from stronger performers. Most firms will already be doing much of what is described. The real value lies in closing the gaps between current practice and leading practice, particularly in two areas:

- From reactive/current-state reporting to forward-looking resilience

- Many firms excel at reporting what is happening now.

- Fewer have structured, documented processes for assessing how medium-term adverse scenarios could affect business model sustainability.

- This is the area where most firms can meaningfully improve without major cost.

- Quality and challenge of information reaching the board

- Boards need concise, decision-useful MI on liquidity, concentration, and resilience, not just raw data.

- Independent challenge is critical, especially in firms where senior management and board roles overlap.

Proportionate application is key.

- Larger, more complex firms should implement deeper scenario analysis and stress testing. Smaller or simpler firms should focus on ensuring core governance, ANLA oversight, and concentration monitoring are robust and well-documented.

Positive takeaway:

- Jersey's TCB and FSB sector continues to demonstrate resilience and high standards of governance. Firms that proactively reflect on these themes will strengthen their sustainability and be well positioned for future supervisory engagement.

Recommended next step for your firm

- Add this item to the next board or risk committee agenda with the action: "Review JFSC Discovery Visit Feedback (June 2026) and agree any enhancements to financial resilience oversight."

APPENDIX 1

What does the Quantitative Snapshot mean?

- Here is a clear, plain-English explanation of the three numbers from the 11 larger trust company and fund services businesses the JFSC visited:

- Average Cost-to-Income Ratio: 80%

What it means:

- For every £100 of income the firms generated, they spent £80 on operating costs (staff salaries, office costs, compliance, systems, professional fees, etc.).

Is 80% good or bad?

- It is reasonable and typical for well-run trust and fund services businesses in Jersey.

- These are people- and compliance-heavy businesses, so costs are naturally high.

- A lower number = more efficient (better).

- A much higher number (e.g. 95%+) would be concerning as it leaves very little profit.

Key takeaway: The firms are profitable and operationally stable, but not unusually lean. This is normal for regulated professional services firms.

- Average ANLA Ratio: 1.85x (well above requirements)

What it means: ANLA stands for Adjusted Net Liquid Assets. It is a Jersey-specific liquidity measure that the JFSC requires trust companies and fund services businesses to maintain.

It shows how much liquid assets (mainly cash or near-cash) the firm holds relative to the minimum the JFSC requires to cover risks and potential outflows.

- 1.85x = On average, these firms held 1.85 times (or 85% more) the minimum liquid assets required.

- “Well above requirements” = They have a comfortable buffer. This is a positive sign of financial resilience.

Why it matters: If a major client leaves or an unexpected cost arises, these firms have enough readily available cash to continue operating without stress. It shows they are managing liquidity prudently.

- Return on Equity (ROE): 29%

What it means: This measures how much profit the firms made for every pound of capital (equity) put in by the owners/shareholders.

- A 29% ROE means that for every £100 of owners' capital, the business generated £29 of profit in the year.

- This is a strong return.

Is 29% good? Yes, it is healthy and above average for this sector.

- It shows the businesses are profitable and making good use of the capital invested in them.

- Many financial services firms aim for ROE in the 15–25% range. 29% indicates strong performance.

Summary – What the JFSC is telling us

Overall message from the JFSC:

- The 11 firms visited are profitable, liquid, and stable. They demonstrate sound financial management. These numbers are illustrative only; they come from larger, more mature firms and are not targets or benchmarks that every firm must hit.

Practical takeaway for your firm

When your board looks at your own numbers, ask:

- Is our cost-to-income ratio stable or creeping up?

- Is our ANLA ratio comfortably above the minimum (with headroom for stress)?

- Is our ROE healthy and sustainable, or is it being supported by one-off items?

These three metrics together give a quick "health check" on efficiency, liquidity resilience, and profitability.

Key documents

- Main announcement: https://www.jerseyfsc.org/news-and-events/jersey-trust-company-and-fund-services-businesses-demonstrate-effective-oversight-and-sound-risk-management/

- Full feedback paper (PDF): https://www.jerseyfsc.org/media/v45ofss2/discovery-visit-feedback-financial-resilience-and-governance.pdf

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.