JFSC NEW GUIDANCE (effective 9/4/26) requires SUSTAINABILITY-RELATED RISK ASSESSMENTS for all registered persons!!

10/04/2026

JFSC sustainable finance guidance note, published APRIL 9, 2026, will support ALL REGISTERED PERSONS in meeting their obligations under their applicable CODE OF PRACTICE in relation to

- Sustainability-related risks and

- Sustainability-related claims.

ALL REGISTERED PERSONS are persons who are registered, or hold a permit or certificate, as applicable, under one or more of the following:-

- Banking Business (Jersey) Law 1991, the Collective Investment Funds (Jersey) Law 1988,

- The Financial Services (Jersey) Law 1998 and the Insurance Business (Jersey) Law 1996

THE JFSC SAYS

- This work supports Jersey’s position as a well-regulated, internationally recognised finance centre and reflects the JFSC's commitment to proportionate, risk-based regulation.

- ALL REGISTERED PERSONS to review the guidance and consider any updates required to their policies, processes and governance arrangements.

THE JFSC SAYS THE GUIDANCE SETS A CLEAR AND CONSISTENT BASELINE ON:

- Identifying, assessing and managing sustainability-related risks, with a particular focus on climate change risks

- Ensuring that sustainability-related claims are fair, clear and not misleading

THE GUIDANCE AND PRINCIPLE 7 IN THE CODES OF PRACTICE

- This guidance applies to all registered persons governed by their “code of practice”

- The full guidance note is available on the JFSC website.

- https://www.jerseyfsc.org/industry/guidance-and-policy/sustainable-finance/

- Principle 7 in the codes of practice

- This guidance, together with the change related to Principle 7 in the codes of practice,

- Will take effect in Q1 2027, giving firms a sufficient transition period to prepare.

SUSTAINABLE FINANCE GUIDANCE

- Issued: 09 April 2026 Effective from: 09 April 2026

- https://www.jerseyfsc.org/industry/guidance-and-policy/sustainable-finance/

Is made up of two parts:

- PART 1 - SUSTAINABILITY RISK MANAGEMENT GUIDANCE

- PART 2 - ANTI‑GREENWASHING GUIDANCE

The JFSC SAYS

- This guidance sets a clear, consistent baseline for managing SUSTAINABILITY-RELATED RISKS, with a focus on:

- Climate change risks and on

- Sustainability-related claims by firms in Jersey.

- It is designed to support firms in meeting their existing obligations under the codes of practice in two areas:

- Principle 3: identifying, assessing and managing sustainability-related risks, with a focus on climate change

- Principle 7: ensuring that any sustainability-related claims are fair, clear and not misleading

- Its approach is proportionate, aligns with recognised international standards, and supports Jersey’s reputation as a well-governed financial centre.

HERE IS THE GUIDANCE WITH EMPHASIS AND MINOR CHANGES FOR EDITORIAL REASONS

1 Sustainability risk management

1.1 Purpose and scope

- This section supports compliance with Principle 3 of the codes of practice by setting practical guidance for how firms can identify, assess and manage sustainability-related risks, with a focus on climate change.

REQUIRED

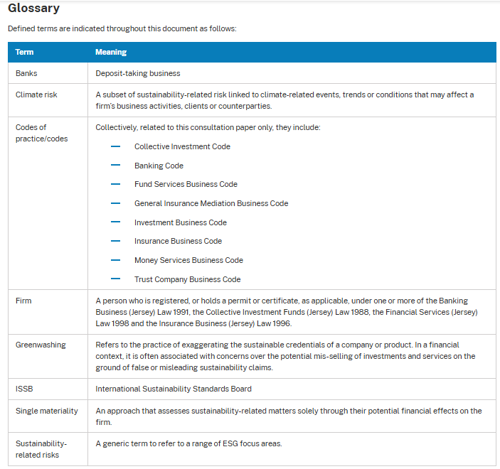

- a SINGLE FINANCIAL-MATERIALITY LENS, consistent with the International Sustainability Standards Board (ISSB).

- This means that the focus is on how climate change may influence a firm’s

- Financial position,

- Performance or

- Cash flows.

NOT REQUIRED

- A double-materiality assessment IS NOT REQUIRED, but firms are able to undertake such an assessment if desired

- A double-materiality assessment means also assessing the firm’s impact on the environment.

1.2 Code requirements

- Principle 3 expects firms to

- Identify, consider and adequately manage THE RISKS they face.

- Sustainability-related risks, particularly climate change risks, should form part of this work.

- Principle 3 DOES NOT require a separate governance framework for sustainability risk.

- As such, this guidance aims to help firms integrate such risks into their existing risk management frameworks under the codes.

1.3 Key definition

- Sustainability-related risks may arise from a range of

- Environmental,

- Social and

- Governance factors.

CLIMATE-CHANGE RISK

- This guidance focuses on CLIMATE-CHANGE RISK as the most immediately material category.

- Climate risk: a SUBSET OF SUSTAINABILITY RISK arising from climate-related events, trends or conditions. Examples include:

- Physical risks:

- Damage or disruption from acute or chronic climate events (for example severe weather, flooding, heat stress) that may impair assets, supply chains or operations

- Transition risks:

- Financial impacts from changes in policy, regulation, technology, markets or preferences associated with the transition to a lower‑emissions or more resource‑efficient economy (for example asset re‑pricing, credit deterioration in exposed sectors, higher input costs)

1.4 Baseline good practice

- The following are non-exhaustive options to support firms in considering climate change risk.

- Firms should consider the following:

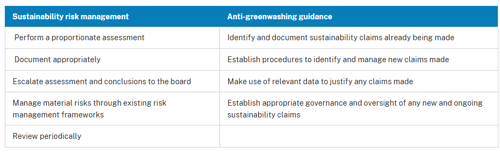

- Assess climate risks as part of their ordinary risk management processes, focusing on material financial impacts.

- Document the assessment of climate risks in a manner proportionate to the business.

- Escalate the assessment and conclusions to the board (or equivalent) for oversight and direction.

- If the board concludes that risks are not material, no further action is required, other than periodic review.

- Where risks are material, the board should set proportionate risk management responses within existing frameworks.

Existing governance and responsibilities

- The board oversees financial risks –

- It seeks and challenges information to understand implications for strategy, the business model and financial resources, and instructs management to maintain proportionate controls

- Clear allocation of responsibilities

- Should exist for day‑to‑day management (for example through existing risk committees or accountable individuals),

- with defined escalation and periodic reassessment mechanisms

- Senior management should

- Ensure they have the skills and resources needed to carry out assessments (for example targeted training where relevant) and

- Keep them under review

Integration into existing frameworks

- Climate change risks should sit within existing governance, risk management and internal control processes, rather than stand apart from them.

- Integration may include:

- Mapping climate change RISK DRIVERS

- To current risk categories (credit, market, liquidity, operational, strategic, reputational) and

- Reflecting RISK DRIVERS in the risk register

- Using existing risk-

- Appetite statements,

- Metrics and

- Limits where appropriate

- Including climate-change considerations in

- Product approval,

- Outsourcing or vendor oversight, and

- Internal audit or review cycles where relevant

Proportionality in practice

- Firms should tailor their efforts and activity to the level of risk they’ve identified.

- Examples include:

- Less material risk

- A qualitative, desktop assessment conducted every 3 years (or on material change)

- For firms with the lowest level of complexity where risks do not ordinarily change, an assessment once every three years is generally acceptable.

- A short board paper

- Simple monitoring of key risk indicators

- More material risk

- Deeper analysis

- Clearer metrics and limits within management information

- Periodic monitoring of risk and board reporting

- Firms may find it helpful to refer to recognised standards such as the ISSB framework when considering the scope and depth of their assessment.

- Documentation and evidence

- It may help firms to keep proportionate records, such as:

- The risk assessment (scope, methodology, judgements on materiality, and conclusions)

- Board papers or minutes evidencing oversight and direction

- Any metrics, limits or controls adopted, and the schedule for periodic review

1.5 Supervisory approach

- JFSC supervisory engagement on climate risk will be proportionate.

- When supervising a firm’s approach, JFSC will

- Generally, look at whether the firm has taken reasonable steps, consistent with baseline good practice OUTLINED IN SECTION 1.4 [ABOVE], to identify, assess and manage climate-change risks within its existing frameworks.

1.6 Operating beyond baseline practice

- Some firms will go beyond JFSC recommended good practice outlined in this guidance.

- This may arise for various reasons including voluntary commitments, group-level obligations or situations where one or more sustainability-related risk has been identified which merit further investigation and management.

- Firms may find it helpful to refer to the ISSB standards for further guidance where other sustainability-related risks are identified as financially material.

Part 2

2 ANTI‑GREENWASHING GUIDANCE

2.1 Purpose and scope

- This section provides practical guidance to help firms so that they take reasonable steps to ensure that sustainability-related claims about the firm, its products or services are fair, clear and not misleading, and that firms can support such claims with evidence.

- It applies to claims made through websites, marketing, investor or client reports and social media.

- The intention is not to deter firms from making sustainability-related claims. It is to ensure claims are presented in a clear, fair and accurate way, consistent with Principle 7.

Definitions

- For the purposes of this guidance, references to

- “Sustainability claims” relate specifically to claims about environmental or social characteristics.

- Greenwashing is

- The practice of misrepresenting those claims to make them seem more sustainable than they actually are.

2.2 Code requirements

- Code requirements 2021

- Anti-greenwashing provisions apply to

- Certified funds (via CIF code),

- Fund services businesses (via FSB code),

- Jersey private funds (JPFs) and

- JPF service providers (via JPF guide) and

- Investment businesses providing advice (via IB code).

- These codes address transparency around sustainability-related characteristics of products.

- Core disclosure requirements for funds

- ‘When a fund or JPF is marketed as investing in sustainable investments, disclosures (via website, prospectus, pre-contractual documents or subscription agreements) must include:

- Alignment with any specific taxonomy (or state if none applies)

- The proportion of sustainable investments

- The basis on which due diligence, benchmarking, performance measurement, and reporting are conducted

- Limitations to methodologies and data

- Investment business requirements

- ‘When a registered person provides investment advice to its Client in relation to a fund that is marketed on the basis of investing in a Sustainable Investment as part of its investment objective, the registered person must

- Inform, and make available to the Client, the appropriate disclosure information in relation to the sustainable investment strategy and objectives of the fund.

- If no such disclosure information is available, the Client must be informed of that fact.’

Code

- From Q1 2027, enhancements to

- Principle 7 (Principle 4 for money services businesses) apply to all registered firms governed by the codes of practice.

- Included within sections 7.2, 7.3, or 7.6 , depending on the codes of practice.

- The following wording will be added, noting there will be sector specific amendments to include references to the fund and permit holder where applicable:

- ‘Sustainability-related claims regarding the registered person, products or services, must be backed by robust evidence and must not be unclear, misleading or unfair.’

This guidance helps firms meet these expectations.

2.3 Core principles for sustainability‑related claims

- Firms may find the following principles helpful when forming or reviewing claims:

- Correct and capable of substantiation

- Claims must be factually accurate and supported by reasonable, verifiable evidence available on request (such as date sources, methods, third‑party assurance where used).

- Firms should keep evidence current and update claims when material changes occur.

- Clear and understandable

- Use plain language that fits the audience. Define terms such as “green”, “sustainable” or “net zero.”

- Avoid vague or aspirational statements without specifics.

- Complete and balanced

- Do not omit important information, limits or trade‑offs (such as thresholds, exclusions, scope of emissions covered or known uncertainties).

- Visuals must reflect the true position.

- Fair and meaningful comparisons

- Comparisons must be between like‑for‑like products or services, with clear bases, methods and time periods.

- Avoid selective or market‑wide claims built on partial samples.

2.4 Applying the principles across the product or service lifecycle

Firms may find it helpful to consider how sustainability-related claims are formed, governed and communicated throughout the product or service life cycle.

Areas that may be relevant include:

- Design and approval

- Document the sustainability claim clearly, including its intended meaning, the evidence required to support it, and the governance arrangements for reviewing, updating or retiring the claim

- Distribution and communication

- Ensure staff and intermediaries understand the claim and its limitations and evidentiary basis

- keep messages consistent across channels and reflect the substance of the claim

- Marketing

- Avoid undefined labels and imagery suggesting benefits without substantiation

- Define any screens, metrics and objectives used

- Firms should ensure that any implied sustainability features can be evidenced and accurately reflect the product’s characteristics

- Data and disclosures

- Claims must be factual and supported by verifiable data and evidence

- Firms should be able to demonstrate the source, completeness, and uncertainty for any data used

- Any limitations or shortcomings in the data underpinning a claim should be clearly disclosed to ensure the accuracy and level of uncertainty are transparent

- Governance and oversight

- Allocate responsibility for reviewing, approving and overseeing claims

- Embed checks within existing risk, compliance or product governance processes

- Maintain an escalation route for concerns

- Ongoing review

- Periodically assess whether the claims remain accurate and appropriate

- Amend or withdraw claims when underlying information changes

- Track progress on long-term targets

2.5 Records and evidence

- Firms should keep proportionate records that show how claims were reviewed and approved, what evidence they used, and how they explained limitations.

2.6 Common pitfalls to avoid

- Areas that may give rise to misunderstanding include:

- Use of broad terms such as “eco‑friendly”, “sustainable”, “fossil‑fuel free” without defining scope, thresholds or exceptions

- Over‑reliance on third‑party ratings or labels without understanding their method or ensuring they align with the stated claim

- Visuals or colour schemes that imply unsupported benefits

- Comparisons that are not like-for-like or based on selective data

2.7 Supervisory approach

- Supervisors will typically consider whether sustainability-related claims meet existing conduct requirements.

- Firms that support claims with evidence, communicate them clearly and completely, and update them when needed, should meet expectations.

2.8 Summary – guidance at a glance

Source

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.