JFSC Guidance Note 7 CHANGES and 3 RETIREMENTS – June 2026 Briefing

08/06/2026

The Jersey Financial Services Commission (JFSC) has revised 7 guidance notes effective 4–5 June 2026 and retired 3.

These updates do not introduce any new Code requirements. They are designed to:

- Clarify how existing requirements should be understood and applied in practice.

- Remove historic or redundant implementation material that is no longer needed.

- Improve consistency, clarity, and usefulness across the guidance suite.

- Support the JFSC's broader programme to simplify the regulatory framework (2026–27 Business Plan).

Impact on Registered Persons:

- Minimal immediate compliance burden.

Firms should

- Review updated guidance relevant to their activities (particularly Investment Business and Trust Company Business), and

- Update internal procedures, training, and documentation where clarifications affect current practices (e.g., vulnerability assessments, suitability processes, conflict management, and compliance monitoring).

Key Themes Across Updates

- Investment Business focus: Enhanced practical guidance on conflicts of interest, suitability (including digital/automated advice, ESG, vulnerability), benchmarking presentation, and support for vulnerable clients.

- Consumer protection & vulnerability: Clearer expectations on identifying hidden/changing vulnerability, adapting communications, and ensuring suitability assessments remain robust.

- Operational clarity: Streamlined guidance on compliance monitoring (with thematic exam insights) and consolidation of Managed Trust Company Business material.

- Housekeeping: Removal of obsolete sanctions references and retirement of redundant/outdated guidance notes.

Detailed Summary of Updates

1. Directions issued to financial services businesses - Last revised: 5 June 2026 | Change: Update

- All references to the Money Laundering and Weapons Development (Directions) (Iran) (Jersey) Order 2015 have been removed.

- These directions ceased to have effect 12 months after being issued.

- https://www.jerseyfsc.org/industry/international-co-operation/sanctions/directions-issued-to-financial-services-businesses/

2. Conflicts of interest requirements under Principle 2 – Code of Practice for Investment Business - Last revised: 4 June 2026 | Change: Update

- Core conflicts requirements remain unchanged. Guidance has been clarified and streamlined, with improved focus on:

- Disclosure requirements and limitations

- Managing residual client risk

- Suitability considerations in conflicts scenarios

- Prioritising avoidance and mitigation over disclosure alone

- https://www.jerseyfsc.org/industry/guidance-and-policy/conflicts-of-interests-requirements-under-principle-2-the-code-of-practice-for-investment-business/

3. Benchmarking under the Codes of Practice for Investment Business - Last revised: 4 June 2026 | Change: Update

- Additional clarification added on the presentation of benchmarking performance, with emphasis on:

- Transparency of assumptions used

- Clear treatment of fees

- Distinction between actual performance and back-tested performance

- https://www.jerseyfsc.org/industry/guidance-and-policy/benchmarking-under-the-codes-of-practice-for-investment-business/

4. The provision of investment services to vulnerable persons (under the Investment Business Code) Last revised: 4 June 2026 | Change: Update

- Guidance clarified to help firms identify and respond appropriately to vulnerability under existing Code requirements. Key areas addressed:

- Identification of hidden or changing vulnerability

- Adapted communications and client engagement

- Suitability assessments for vulnerable clients

- Systems, controls and record-keeping expectations

- Use of alternative effective approaches that still meet IB Code requirements

- https://www.jerseyfsc.org/industry/guidance-and-policy/the-provision-of-investment-services-to-vulnerable-persons-under-the-code-of-practice-for-investment-business/

5. Suitability of advice under the Code of Practice for Investment Business - Last revised: 4 June 2026 | Change: Update

- Core suitability requirements remain unchanged. Practical updates cover:

- Digital or automated advice models

- Incorporating vulnerability considerations into suitability assessments

- ESG / sustainability-related recommendations

- Content and use of suitability letters

- What firms should evidence, provide to clients, retain on file, and periodically review

- https://www.jerseyfsc.org/industry/guidance-and-policy/suitability-of-advice-for-investment-business/

6. Compliance Monitoring Last revised: 4 June 2026 | Change: Update

- Updated to help firms better contextualise and design their compliance monitoring plans.

- Includes practical scenarios drawn from recent compliance monitoring thematic examinations conducted by the JFSC.

- https://www.jerseyfsc.org/industry/guidance-and-policy/compliance-monitoring/

7. Managed Trust Company Business Last revised: 4 June 2026 | Change: Update

- Guidance has been consolidated and simplified. Material from related guidance notes of the managed trust company has been incorporated.

- The related standalone guidance on distinguishing between managed trust company and participating member has been retired (see below).

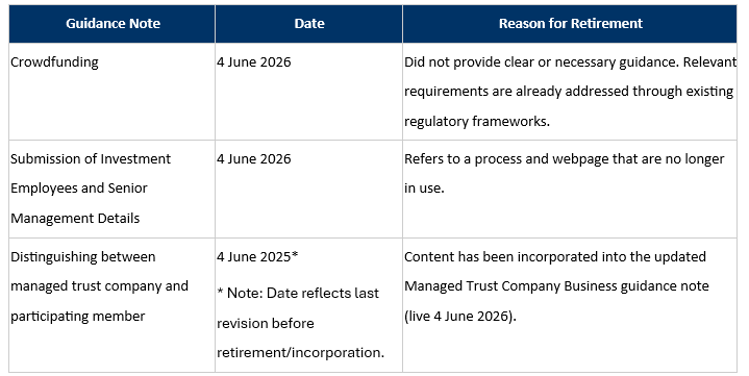

Retired Guidance Notes

The following guidance notes have been withdrawn as part of the simplification programme. Firms should ensure any internal references or processes are updated accordingly.

Implications & Recommended Actions

For Investment Business firms:

- Review and update policies/procedures on conflicts of interest, suitability assessments, and vulnerable client handling.

- Ensure benchmarking disclosures meet the new transparency expectations (assumptions, fees, actual vs back-tested).

- Consider enhancements to suitability letters, evidence files, and ongoing review processes, particularly for digital advice and ESG recommendations.

- Strengthen systems and controls for identifying and responding to vulnerability (including hidden/changing circumstances).

For Trust Company Business / Managed entities:

- Familiarise teams with the consolidated Managed Trust Company Business guidance.

- Update any internal references to the retired "distinguishing" note.

For all registered persons:

- Remove any internal references to the retired Crowdfunding and Investment Employees submission guidance.

- Update compliance monitoring plans to reflect the new practical scenarios and contextual guidance.

- Consider whether existing training materials need refreshing in light of the clarifications (especially vulnerability and suitability).

Next Steps:

- Access the full updated guidance notes and supporting materials directly from the JFSC website. Please share feedback on clarity or navigation using the channels below.

Sources & Further Information

Official JFSC pages (recommended reading):

- Guidance Note Changes: https://www.jerseyfsc.org/industry/simplifying-our-regulatory-framework/guidance-note-changes/

- Simplifying our Regulatory Framework programme: https://www.jerseyfsc.org/industry/simplifying-our-regulatory-framework/

- https://www.jerseyfsc.org/industry/simplifying-our-regulatory-framework/

- https://www.jerseyfsc.org/industry/simplifying-our-regulatory-framework/guidance-note-changes/

- Feedback / Consultation: policy@jerseyfsc.org or online survey

Disclaimer

This briefing note is prepared for informational purposes only and does not constitute legal, regulatory, or compliance advice. Registered persons should refer directly to the official JFSC guidance and consult their compliance or legal advisors as appropriate. While every effort has been made to ensure accuracy, users should verify information against the primary sources on the JFSC website.

Briefing prepared: 8 June 2026 | Based on JFSC publications as of 5 June 2026

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.