JFSC Feedback from Transaction Monitoring Questionnaire [no visit thematic report]

26/10/2021

Running parallel to a Transaction Monitoring virtual-visits programme in Q3/2021, the JFSC, in July 2021, asked 25 businesses to complete a Transaction Monitoring Questionnaire [QUESTIONS BUT NO VISIT]

The purpose of the questionnaire was to provide the JFSC with an understanding on

- The methods used to monitor transactions and

- Their relevant systems and controls (including policies and procedures).

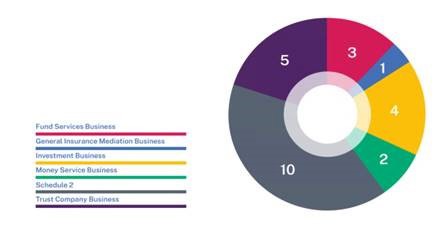

The sample of 25 relevant persons included regulated businesses from the following sectors:

- Fund services business (FSB), investment business (IB) and trust company business (TCB).

- Schedule 2 businesses: lawyers, estate agents, casinos, and lenders.

Breakdown of the QA is as follows:

The questionnaire explored compliance with the following matters

- All relevant persons are required by the Order to

- Ensure that systems and controls are established to enable the identification and scrutiny of:

- Complex or unusually large transactions

- Unusual patterns of transactions which have no apparent economic or visible lawful purpose

- Any other activity that a relevant person regards as particularly likely by its nature to be related to the risk of money laundering.

2. The Order also sets out:

- That on-going monitoring must involve amongst other things, scrutinizing transactions undertaken throughout the course of a business relationship, to ensure that the transactions being conducted are consistent with the relevant person’s knowledge of the customer, including

- The customer’s business and risk profile (including where necessary, the source of the funds).

3.The relevant Handbooks for the Prevention and Detection of Money Laundering and Countering the Financing of Terrorism (the Handbooks) set out regulatory requirements for relevant persons to

- Scrutinise transactions

- Monitoring activity and:

- Demonstrate that transaction and activity monitoring arrangements and associated systems and controls are adequate and effective.

The Transaction Monitoring Questionnaire [QUESTIONS BUT NO VISIT] report is out

- The JFSC have now issued their findings report – https://www.jerseyfsc.org/media/4938/20211022-transaction-monitoring-feedback-paper-web-final.pdf -

- And in this report they suggest the report provides meaningful feedback which Boards and senior management should consider against their own arrangements, then take action where necessary to enhance their systems and controls.

The report highlights the x25 firms’ Manual vs automated approaches as follows

- No relevant persons used a fully automated approach to transaction monitoring with:

- x17 (68%) confirming they use manual transaction monitoring methods both before and after a transaction has taken place.

- X8 (32%) of the relevant persons confirmed that they used a mix of manual and automated transaction monitoring processes.

- When using automated monitoring methods,

- X7 relevant persons confirmed their automated processes operated in real-time.

- X18 relevant person’s automated monitoring solution scrutinised transactions post-event.

THE REPORT’S EXECUTIVE SUMMARY SHOWS GOOD AND BAD PRACTICES

Highlighted deficiencies

Several deficiencies were highlighted by relevant persons relating to existing systems and controls:

- One respondent indicated that no routine transaction monitoring was undertaken

- Four respondents highlighted that their systems and controls did not require them to record the findings from transaction monitoring reviews

- Seven respondents confirmed that there were backlogs in reviewing transactions or related processes

- Three respondents indicated that they had identified deficiencies in the oversight of their transaction monitoring processes

- Four respondents indicated that they had identified matters in their transaction monitoring policies and procedures that required addressing

- Four respondents confirmed that training in relation to transaction monitoring did not take account of Jersey requirements.

Highlighted good practice

- There were two areas where a majority of relevant persons that received the questionnaire highlighted areas of best practice in their approaches to scrutinising transactions and monitoring activity:

- › 68% of respondents confirmed that once a transaction monitoring review had been undertaken, they required a second reviewer to sign off its completion

- › 53% indicated that transaction monitoring methods were tested before going live.

Enhancements to consider Boards and senior management should consider the following actions, to enhance their systems and controls:

- Routine monitoring must be undertaken

- Systems and controls must record findings arising from transaction monitoring reviews

- Where there are backlogs in reviews, deficiencies in oversight, or identified matters that need to be addressed, business should:

- Escalate to the appropriate level of management

- Put plans in place to resolve these matters

- Action these plans in a timely manner.

- Training in relation to transaction monitoring must take account of Jersey requirements

- A second reviewer’s sign off on transaction monitoring reviews should be considered

- Transaction monitoring methods should be tested before going live.

Follow-on actions

- As a result of the findings from this questionnaire, follow-on supervisory engagement will take place with certain relevant persons.

- This may include formal remediation plans being agreed, or other supervisory action appropriate to the particular circumstances

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.