JERSEY do you know what risk assessments you need to have as a business [P.S. NOT JUST ML!!!!]

07/05/2026

In Jersey (Channel Islands, UK), several key laws, regulations, and regulatory codes of practice mandate risk assessments in specific contexts.

These align closely with the examples you provided (data protection, health and safety, money laundering, and regulated activities). Jersey operates its own legal framework as a Crown Dependency, independent of the UK or EU, but its rules are often aligned with international standards (e.g., FATF for AML, GDPR-equivalent for data protection).

Risk assessments are generally required to identify, evaluate, and mitigate risks to people, data, businesses, or compliance obligations. They must typically be documented (in many cases), kept up to date, and made available to the relevant authority on request. Failure to comply can result in enforcement action, fines, or criminal offences.

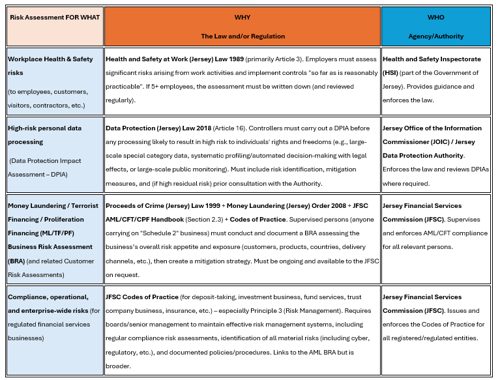

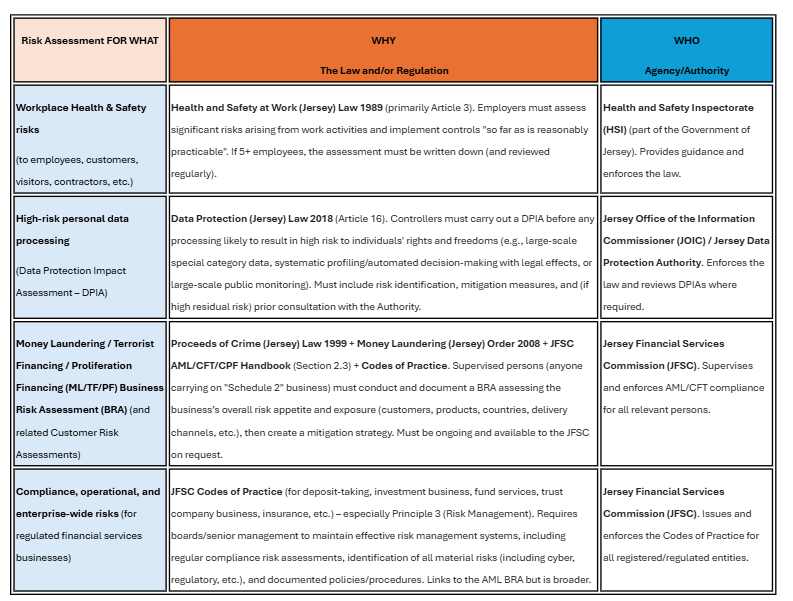

Below is a summary table of the main requirements. It focuses on the core mandatory areas you referenced, based on official Jersey sources (e.g., gov.je, JFSC, and the Jersey Office of the Information Commissioner).

Additional Notes on Requirements and Best Practices

- Who must comply? Employers (H&S), data controllers/processors (DPIA), and "supervised persons"/regulated entities (AML and Codes of Practice). Even “sole” traders or small businesses have basic duties in H&S and AML if they fall under Schedule 2 activities.

- Documentation & Review: Most require written records (especially if 5+ staff for H&S or for regulated firms). Reviews must be periodic or triggered by changes (e.g., new processes, incidents, or regulatory updates).

- Best Practices (recommended, not always strictly mandatory):

- Follow official guidance (e.g., HSI’s 5-step risk assessment process, JOIC DPIA templates/checklists, JFSC Handbook examples).

- Integrate risk assessments into a wider risk management framework (e.g., ISO 31000 principles are commonly referenced as good practice by JFSC-regulated firms).

- For regulated entities, the JFSC expects the BRA and compliance risk assessments to be board approved and linked to the business’s overall strategy.

- Sector-specific rules may add extra layers (e.g., care homes under the Care Commission or education settings may reference H&S plus additional minimum standards).

These are the primary areas that legally require risk assessments in the contexts you mentioned. Other niche areas (e.g., fire safety, environmental permits, or cyber under the emerging Cyber Security (Jersey) Law 2025) may impose related duties, but they are usually covered under the above frameworks or specific licences.

For the most current official guidance or templates:

- Health & Safety: gov.je (HSI pages)

- Data Protection: jerseyoic.org (DPIA portal and checklists)

- AML & Regulated Activities: jerseyfsc.org (AML Handbooks and Codes of Practice)

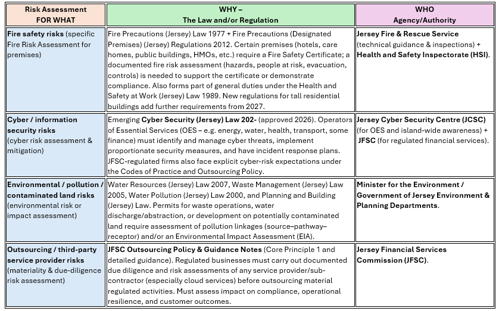

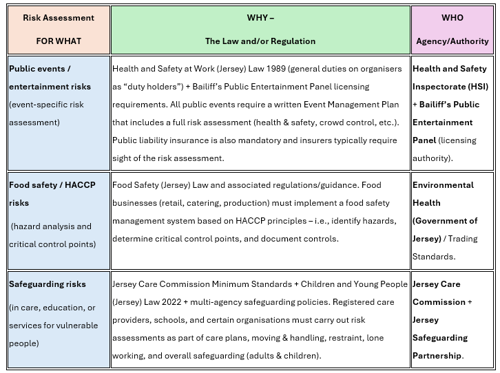

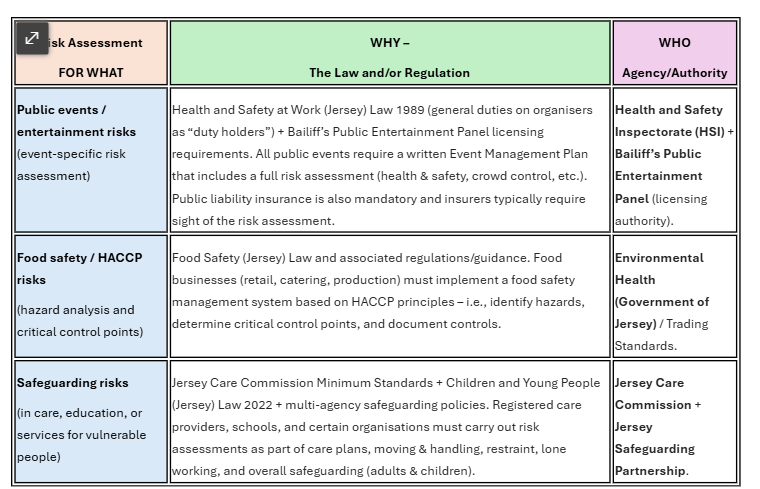

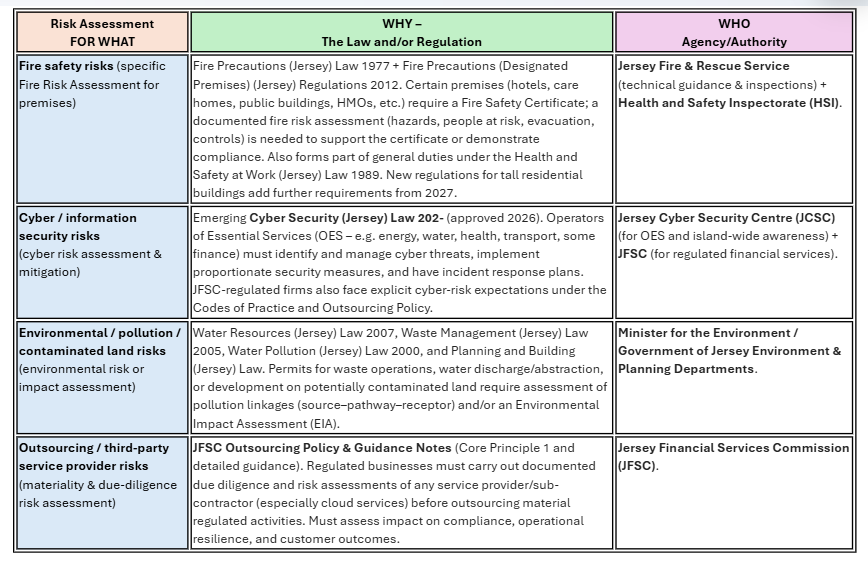

Several additional (niche or sector-specific) drivers for risk assessments in Jersey.

These build on or sit alongside the core ones (Health & Safety at Work Law, Data Protection Law, AML/CFT, and JFSC Codes of Practice). They are often triggered by licensing, permitting, or specific regulatory expectations rather than a single “risk assessment” statute.

I have focused on the examples you mentioned (fire safety, environmental permits, cyber, outsourcing, public events/insurance) plus a couple of other common ones. All are based on current Jersey legislation, guidance, and regulatory policy (as of May 2026).

Quick additional notes on “best practice” vs legal requirement

- Many of these are not standalone “risk assessment laws” but are embedded in licensing/permit conditions or flow from broader duties (especially H&S). Failure to produce a suitable assessment can still lead to enforcement, refusal of a licence/permit, or civil liability.

- Insurance angle: Public-liability or employers’ liability insurers routinely require evidence of suitable risk assessments (fire, events, cyber, etc.) before issuing or renewing cover – this is commercial best practice rather than a statutory rule.

- Review & documentation: Almost all require the assessment to be written, kept up to date, and available for inspection. Competent persons must usually carry them out.

- Emerging / sector-specific: Climate-related financial risk disclosures and sustainability risk assessments are also becoming expected for larger JFSC-regulated firms (aligned with international standards).

Reference List (all sources)

Copy the entire block below if you want every link in one go:

- Health & Safety at Work (Jersey) Law 1989: https://www.jerseylaw.je/laws/current/l_8_1989

- HSI Guidance: https://www.gov.je/Industry/HealthSafetyWork/HSI/Legislation/LawRegulations/pages/guidancehswlaw.aspx

- Data Protection (Jersey) Law 2018: https://www.jerseylaw.je/laws/current/l_3_2018

- JOIC (DPIA): https://jerseyoic.org/

- JFSC AML/CFT/CPF Handbook: https://www.jerseyfsc.org/industry/financial-crime/amlcftcpf-handbooks/amlcftcpf-handbook/

- JFSC Codes of Practice: https://www.jerseyfsc.org/industry/codes-of-practice/

- Fire Precautions (Jersey) Law 1977: https://www.jerseylaw.je/laws/current/l_8_1977

- Jersey Fire & Rescue Service Fire Safety Legislation: https://jerseyfire.je/your-safety/protection/fire-safety-legislation

- Cyber Security (Jersey) Law 202– & Policy Framework: https://www.gov.je/SiteCollectionDocuments/Industry%20and%20finance/Cyber%20Policy%20Framework%20Consultation-July%202025.pdf

- JFSC Outsourcing Policy: https://www.jerseyfsc.org/industry/guidance-and-policy/outsourcing-policy/

- Public Events H&S Guidance: https://www.gov.je/Industry/HealthSafetyWork/HSI/Legislation/General/pages/publicevents.aspx

- Food Safety (HACCP): https://www.gov.je/Industry/RetailHospitality/FoodDrink/pages/foodsafety.aspx

- Environmental / Water Pollution Law: https://www.gov.je/Environment/Water/pages/waterpollution.aspx

- Jersey Care Commission Standards: https://carecommission.je/

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.