iSAR and eSAR Reporting: Lessons from Shah, Parvizi, and the HSBC DIFC $79m Claim

08/04/2026

Executive Summary

- Internal Suspicious Activity Reports (iSAR) and External Suspicious Activity Reports (eSAR/eSAR) are core to a bank’s anti-money laundering (AML) and counter-terrorist financing (CTF) obligations.

- Please note that some jurisdictions refer to these reports as Suspicious Transaction Reports (STRs) – this briefing still applies.

- While the legal threshold for “suspicion” is deliberately low, mismanagement of the iSAR → eSAR chain, particularly prolonged freezes under the “no consent” regime, exposes banks to high-value customer litigation, regulatory scrutiny and reputational damage.

- Two landmark English cases and a current DIFC case illustrate the risks:

- Shah v HSBC Private Bank (UK) Ltd ([2010] EWCA Civ 31 & [2012] EWHC 1283 (QB))

- Customer claimed over US$300 million in losses from SAR-related delays.

- Iraj Parvizi v Barclays Bank Plc ([2014] EWHC B2 (QB))

- Professional gambler’s account freeze led to a claim that was ultimately struck out.

- The current HSBC Bank Middle East Limited (HBME) DIFC claim

- US$79 million, filed 9 March 2026 by Nazma Begum, Amar Khan and Jakob International Inc is the latest high-profile example.

- A 2013 Guernsey-branch eSAR (triggered by a 2012 Middle East relationship) resulted in an 11+ year freeze.

- The funds were declared clean in Guernsey in 2024, yet the claimants are now pursuing damages in the DIFC against the Dubai-based HBME entity.

ANALYSIS REPORT

1. Introduction and Context

- Banks face a statutory duty to report suspicion of money laundering while also owing contractual and common-law duties to customers.

- The iSAR/eSAR regime attempts to balance these obligations, but poor governance, inadequate review cycles or “defensive AML” practices can turn a compliance safeguard into a litigation trigger.

- The HBME DIFC case demonstrates how a single eSAR filed in one jurisdiction (Guernsey) can lead to multi-jurisdictional claims against another group entity (HBME in Dubai) years later.

2. The iSAR / eSAR Process Explained

- iSAR (Internal SAR): Any staff member who forms a reasonable suspicion must escalate it internally to the Money Laundering Reporting Officer (MLRO) or nominated officer. This is the firm’s first line of defence and must be documented contemporaneously.

- eSAR / eSAR (External SAR): Only the MLRO can file the formal report with the Financial Intelligence Unit (FIU), e.g., Guernsey FIU, Jersey JFCU or UK National Crime Agency (NCA). Filing grants statutory protection (safe harbour) from money-laundering offences.

In Guernsey and Jersey, the practice of the distinction is explicit:

- iSAR protects the individual reporter; eSAR triggers the “consent regime” and potential “no consent” freeze.

- Typical timeline: iSAR raised → MLRO investigates (without tipping off) → eSAR filed (or not) → FIU responds with consent or “no consent”.

3. Legal Framework and “Suspicion” Threshold

Under the Proceeds of Crime Act 2002 (UK) and equivalent offshore legislation (e.g., Guernsey Disclosure Law 2007):

- “Suspicion” is more than a vague feeling of unease but does not require reasonable grounds, firm evidence or even a clear target (confirmed in Parvizi).

- Once a genuine SAR is filed, the bank is protected from tipping-off offences and money-laundering liability.

- However, the bank may still face civil claims for breach of mandate or negligence if the freeze is disproportionate or not reviewed.

4. Key Litigation Precedents

Shah v HSBC Private Bank (UK) Ltd Customer instructed large transfers; the bank filed multiple SARs and delayed execution. Claim for >US$300 million in lost opportunities.

- Court of Appeal (2010): Bank must prove at trial that suspicion was genuinely held; summary judgment inappropriate.

- High Court (2012): Claim ultimately dismissed after full trial, but the case lasted 3> years and was extremely costly.

- Key lesson: Even protected SARs can lead to expensive disclosure battles and damages claims if the freeze is not managed proportionately.

Iraj Parvizi v Barclays Bank Plc [2014] EWHC B2 (QB)

- Professional gambler’s accounts frozen after a SAR.

- Claim for lost betting profits struck out.

- Court held genuine (honestly held) suspicion is sufficient to defeat a breach-of-contract claim; the threshold is deliberately low.

- Key lesson: Banks are strongly protected where suspicion is documented and honest, but the process must still be defensible in court.

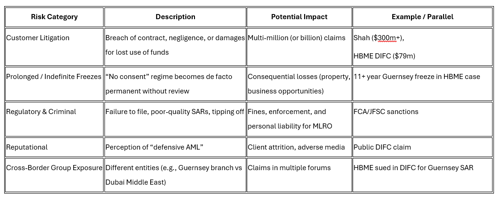

5. Risks of Poor iSAR/eSAR Management

6. Application to the HBME DIFC $79m Claim

- 2012: Dubai relationship manager (Katharine Lisle) advises on $10m transfer.

- April 2013: Jakob Account opened with HSBC Private Bank (Suisse) SA, Guernsey Branch.

- 16 May 2013: Guernsey branch files eSAR → “no consent” freeze.

- 2024: Guernsey Royal Court declares funds not proceeds of crime.

- March 2026: Claimants sue HBME (Middle East entity) in DIFC for $79m damages, alleging root due diligence failures and Group-wide disproportionate freeze.

This is the Shah/Parvizi pattern amplified: clearance in one jurisdiction followed by a high-value damages claim in another against a different group entity.

7. Best Practice Recommendations

- Robust iSAR documentation, contemporaneous notes, and clear rationale.

- Timely and proportionate MLRO review of long-running “no consent” cases.

- Consider less intrusive measures (partial consent, monitored accounts).

- Clear Group-wide policies on cross-border SAR coordination.

- Regular training and scenario testing for relationship managers and MLROs.

- Maintain litigation-ready audit trails for every SAR.

- Periodic independent assurance of SAR governance.

8. Conclusion and Key Takeaways

- iSAR/eSAR reporting is not a “tick-box” compliance exercise.

- Poor management turns a statutory protection into a litigation liability.

- The HBME DIFC case, like Shah and Parvizi before it, shows that even genuine suspicions can lead to massive claims if the freeze is not reviewed or managed proportionately across the Group.

- Firms should treat every iSAR as potentially litigious and ensure governance, documentation and review cycles are court-ready.

9. Sources (WWW) –

- https://www.casemine.com/judgement/uk/5a8ff71560d03e7f57ea7419 Shah & Anor v HSBC Private Bank (UK) Ltd (Court of Appeal 2010)

- https://www.lexology.com/library/detail.aspx?g=063d98ce-8563-4659-8963-59d85c01b18c Shah v HSBC [2012] EWHC 1283 (QB) High Court summary

- https://www.cliffordchance.com/content/dam/cliffordchance/briefings/2011/11/suspicious-minds-court-of-appeal-rules-on-disclosure-in-challenges-by-customers-to-sars-shah-v-hsbc-private-bank-uk.pdf Clifford Chance briefing on Shah disclosure issues

- https://www.bailii.org/ew/cases/EWHC/QB/2014/B2.html Full Parvizi v Barclays Bank Plc [2014] EWHC B2 (QB) judgment

- https://www.lexology.com/library/detail.aspx?g=9bf2ce45-df05-4c3b-a932-3f07fcf1f111 Lexology summary of Parvizi case

- http://www.comsuregroup.com/news/its-time-to-spring-clean-your-isar-esar-and-sancsar-policies-and-training-programs/ Guernsey/Jersey iSAR/eSAR guidance

- https://guernseylegalresources.gg/CHttpHandler.ashx?documentid=63278 2016 Guernsey judgment (Jakob International Inc v HSBC) confirming 16 May 2013 SAR

- https://www.mourant.com/updates/recent-guernsey-case-sheds-light-on-the-role-of-a-business-holding-assets-subject-to-a-suspicious-activity-report/ 2024 Guernsey Jakob judgment summary

- https://www.fnlondon.com/articles/hsbc-faces-79m-lawsuit-over-clients-decade-long-assets-freeze-450f2b93 Primary reporting on HBME DIFC $79m claim

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.