Federal Court Dismisses DPA Case Against Offshore Lender for FATCA and Money Laundering Conspiracy

23/06/2026

In a notable development in cross-border tax enforcement, a federal judge in Brooklyn has dismissed all criminal charges against an offshore bank based in Saint Vincent and the Grenadines.

The dismissal follows the Caribbean lender's successful completion of a deferred prosecution agreement (DPA) resolving allegations of conspiracy to violate the U.S. Foreign Account Tax Compliance Act (FATCA) and a related money-laundering conspiracy.

The case, handled in the U.S. District Court for the Eastern District of New York, cantered on claims that the bank conspired to help U.S. taxpayers conceal assets and evade reporting obligations under FATCA, the 2010 U.S. law designed to prevent Americans from dodging taxes through undisclosed foreign accounts.

What the DPA Required and How It Was Resolved

According to court records, the bank entered into the DPA with the Department of Justice (DOJ) in a prior year. Under the agreement, the institution:

- Acknowledged the alleged conduct in a detailed statement of facts

- Paid a substantial monetary penalty

- Overhauled its anti-money laundering (AML) and FATCA compliance programs

- Cooperated fully with U.S. authorities

- Operated under the oversight of an independent compliance monitor for a set period

After the bank was certified and the government confirmed that it had fully met every obligation, prosecutors moved to dismiss the criminal case.

The court granted the motion, bringing the matter to a close without a conviction.

This outcome is typical of well-structured DPAs in financial crime cases: companies that demonstrate genuine remediation and sustained compliance can avoid the collateral consequences of a guilty plea or conviction.

Background: FATCA and Offshore Banking Scrutiny

- FATCA requires foreign financial institutions (FFIs) to identify and report information on accounts held by U.S. persons to the IRS or face a 30% withholding tax on U.S.-source payments.

- Many Caribbean jurisdictions, including Saint Vincent and the Grenadines, have formal intergovernmental agreements (IGAs) with the United States to implement these rules.

- The law has driven a global shift toward tax transparency. Combined with the OECD's Common Reporting Standard (CRS), it has made it far harder for individuals to hide assets offshore undetected.

- Caribbean financial centres have faced heightened U.S. and international scrutiny over the years for AML and tax compliance shortcomings. Institutions that fall short can face not only civil penalties but, in serious cases, criminal conspiracy charges exactly the path this matter took before the DPA provided an off-ramp.

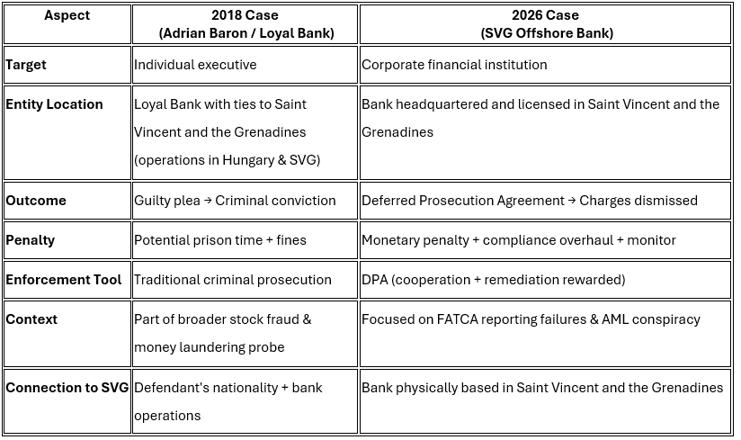

Comparison to the 2018 FATCA Conviction Case

- This 2026 resolution offers a striking contrast to the first-ever criminal conviction under FATCA, which was also prosecuted in the Eastern District of New York (Brooklyn) in 2018.

- In that case, Adrian Baron, a dual UK–Saint Vincent citizen and former Chief Business Officer of Loyal Bank Ltd. (a bank with operations in Budapest, Hungary, and Saint Vincent and the Grenadines), pleaded guilty to conspiracy to defraud the United States by intentionally circumventing FATCA reporting requirements.

Key facts from the 2018 case:

- An undercover FBI agent in Brooklyn, posing as a U.S. citizen involved in a stock manipulation scheme, asked Baron to open offshore accounts without proper FATCA reporting or identification of the U.S. owner.

- Baron complied, helping conceal the accounts and facilitating the movement of funds tied to the fraudulent scheme (including money laundering elements).

- He was extradited from Hungary to face charges in New York.

- This marked the DOJ's first successful FATCA conviction since the law's enactment in 2010. Baron faced up to five years in prison.

Key differences between the two cases:

*"SVG offshore bank" MEANS “Saint Vincent and the Grenadines offshore bank”.

What the comparison reveals:

- The DOJ uses different tools depending on the target and level of cooperation. Individuals who actively assist evasion (especially in undercover stings) face aggressive prosecution and convictions.

- Institutions that self-report issues, pay penalties, implement strong compliance programs, and accept monitoring can resolve matters through DPAs without the lasting stigma of a conviction.

- Both cases underscore the Eastern District of New York's central role in FATCA and offshore tax enforcement.

- The 2026 outcome shows the maturation of FATCA enforcement: from securing the "first conviction" in 2018 to offering structured resolution paths for cooperative institutions in 2026.

- This evolution reflects a more nuanced enforcement strategy, punishing willful individual misconduct while encouraging corporate remediation.

Why This Matters for the Industry

- For the offshore banking sector, the 2026 resolution (especially when viewed alongside the 2018 precedent) sends a clear dual message:

- Accountability is non-negotiable,

- But genuine cooperation and reform can produce a path forward without criminal conviction.

Moving Forward

- The bank in question can now operate without the overhang of pending U.S. criminal charges.

- The case serves as a case study for other offshore institutions in Saint Vincent and the Grenadines and similar jurisdictions.

- As global tax information exchange continues to mature, the incentive remains the same: build and maintain strong FATCA, CRS, and AML controls.

- Those that do are far less likely to find themselves in a Brooklyn courtroom or elsewhere!!.

Sources

2026 Case Background & FATCA in Saint Vincent and the Grenadines

- Agreement between the Government of the United States of America and the Government of St. Vincent and the Grenadines to Improve International Tax Compliance and to Implement FATCA (U.S. Department of the Treasury, August 18, 2015) https://home.treasury.gov/system/files/131/FATCA-Agreement-St-Vincent-and-the-Grenadines-8-18-2015.pdf

- Bank of Saint Vincent & the Grenadines – FATCA Compliance Page https://www.bosvg.com/fatca/

- Government of Saint Vincent and the Grenadines – FATCA (Ministry of Finance) https://finance.gov.vc/finance/index.php/fatca

- Government of Saint Vincent and the Grenadines – FATCA FAQs https://finance.gov.vc/finance/index.php/fatca/faq

2018 FATCA Conviction Case (for comparison)

- U.S. Department of Justice – Former Executive of Loyal Bank Ltd. Pleads Guilty to Conspiring to Defraud the United States by Failing to Comply with FATCA (Eastern District of New York, September 11, 2018) https://www.justice.gov/usao-edny/pr/former-executive-loyal-bank-ltd-pleads-guilty-conspiring-defraud-united-states-failing

- Jones Day – First Conviction in the United States for FATCA Violations (September 2018) https://www.jonesday.com/en/insights/2018/09/first-conviction-in-the-united-states-for-fatca-vi

- Money Laundering News – DOJ Secures First Ever Conviction for Violating FATCA (September 17, 2018) https://www.moneylaunderingnews.com/2018/09/doj-secures-first-ever-conviction-for-violating-fatca/

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.