COMSURE MUSING on the JFSC Proposed Amendments to the Civil Financial Penalty Methodology for Registered Persons [Consultation No. 3 2026]

31/03/2026

EXECUTIVE SUMMARY

- The Jersey Financial Services Commission (JFSC) is consulting on targeted amendments to its published methodology for calculating civil financial penalties imposed on registered persons.

- The natural-persons methodology will be consulted on separately at a later date.

- Key observations

- The overall aim is greater transparency, predictability and consistency while retaining case-by-case flexibility.

- This is largely a clarificatory and alignment exercise rather than a fundamental overhaul.

- It improves transparency and sets clearer expectations around proactive cooperation and remediation while preserving the JFSC’s discretion.

- Firms that already maintain strong compliance cultures and swift response protocols are likely to benefit most from the expanded mitigation guidance.

WHO ARE THE CHANGES AFFECTING DIRECTLY

- Registered persons (as defined in Article 1 of the Financial Services Commission (Jersey) Law 1998) – i.e.

- Banks, insurers (non-Category A), fund service providers,

- Supervised persons under the Proceeds of Crime regime, etc.

- For the avoidance of doubt, supervised persons under the Proceeds of Crime regime, etc., including lawyers, accountants and estate agents, are caught as “registered persons” under the JFSC civil financial penalty methodology

- The glossary on page 13 of the consultation paper defines “registered person” as having the meaning given in Article 1 of the Financial Services Commission (Jersey) Law 1998. That definition explicitly includes:

- A “supervised person” as defined in Article 1(1) of the Proceeds of Crime (Supervisory Bodies) (Jersey) Law 2008

- A “supervised person” is a category of person who carries on relevant professional activities “by way of business” (these are called Schedule 2 businesses under the Proceeds of Crime Law).

- Categories include:- lawyers, accountants and estate agents

CHANGES AND KEY PROPOSALS

- The changes are driven by two main factors:

- Legislative alignment –

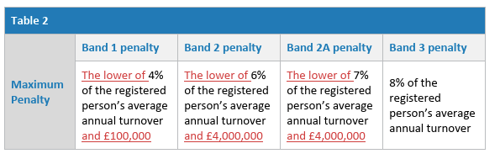

- consequential updates to reflect the Financial Services Commission (Financial Penalties) (Jersey) Amendment Order 2026 (in force 12 March 2026), which re-introduced maximum penalty caps for Bands 1, 2 and 2A (Band 3 remains uncapped).

- Operational experience –

- enhanced, clearer guidance at key steps of the methodology, plus an express reference to the guiding principle of having regard to the best economic interests of Jersey.

- Legislative alignment –

- Key proposals include:

- Fuller non-exhaustive factors for assessing knowledge of a contravention (Step 2),

- Voluntary reporting (Step 3),

- Rectification/prevention of recurrence (Step 4)

- Potential financial consequences (Step 11);

- A reduction in the residual aggravating/mitigating adjustment at Step 5 from ±50% to ±25%;

- Clearer (but non-automatic) guidance on settlement discounts; and

- Removal of worked examples in appendices for a more streamlined document.

THINGS TO LOOK OUT FOR

- Subjective thresholds:

- Terms such as “particularly prompt, transparent and comprehensive” (reporting) and “proactive, timely, comprehensive and demonstrably effective” (remediation) are not defined;

- mitigation is available only where conduct goes beyond what is ordinarily expected to meet statutory/regulatory obligations. Routine compliance will generally be treated as neutral.

- “Best economic interests of Jersey” principle:

- Not scored in Step 1 seriousness; instead addressed (where relevant) at Step 11.

- Impacts must be material, reasonably foreseeable, evidenced and causally linked to the penalty – not speculative.

- The draft gives examples (service continuity, financial exclusion, essential services) but leaves room for interpretation.

- Narrower residual discretion:

- Step 5 adjustment reduced to ±25% (from ±50%).

- This may limit flexibility for factors not captured elsewhere.

- Removal of worked examples:

- The methodology is now more principle-based.

- Firms lose illustrative benchmarks that previously aided predictability.

- Careful monitoring

- In the drafting itself, the proposals are coherent and clearly flagged as consequential or enhancement-driven. However, the interplay between the new dedicated steps (2–4) and the reduced Step 5 range will require careful monitoring once finalised.

RECOMMENDATION:

- Treat the consultation as an opportunity to engage early. Review the Appendix A draft methodology against current internal processes and consider a targeted submission if your organisation has material exposure to enforcement risk or strong views on the economic-interests principle or settlement-discount mechanics.

- The final updated methodology is expected to be published after the JFSC considers feedback.

WHAT SHOULD BE DONE

- Review the proposed revised methodology (Appendix A of the consultation paper – marked-up version).

- Assess internal policies and procedures against the new guidance, particularly:

- Voluntary reporting and cooperation protocols.

- Speed, quality and demonstrable effectiveness of remediation/prevention measures.

- Evidence gathering for Step 11 financial-consequences arguments (including any best-economic-interests’ points).

- Consider submitting a response to the consultation (via the JFSC online form) by 23 April 2026, 4:00pm. Industry bodies should include a summary of the types of entities they represent.

- Brief relevant teams (compliance, legal, senior management) on the heightened expectations for prompt, transparent and comprehensive action to secure mitigation.

- Direct any queries to enforcement@jerseyfsc.org.

SOURCES

- Read the full consultation on amendments to the JFSC’s civil financial penalty methodology for registered persons.

- https://www.jerseyfsc.org/industry/consultations/consultation-on-amendments-to-the-jfsc-s-civil-financial-penalty-methodology-for-registered-persons/

- View the proposed revised methodology at Appendix A.

- https://www.jerseyfsc.org/media/3dggzdys/civil-fin-penalties-rp-metholology-final-draft-march-2026.pdf

ALSO READ

JFSC Consultation launched on the Civil Financial Penalty Methodology for a Registered Person [DL-23 April 2026]

The JFSC has published a consultation on proposed amendments to the JFSC methodology for determining the amount of a civil financial penalty imposed on a registered person.

These changes are intended to align the methodology with recent legislative changes and to improve clarity, transparency, and predictability in its application, while preserving the flexibility needed to address the circumstances of individual cases.

- Read the full consultation on amendments to the JFSC’s civil financial penalty methodology for registered persons

- Submit your response by 4:00pm on 23 April 2026.

Who does this affect?

The proposals may affect

- Registered persons subject to the JFSC civil financial penalties regime,

- Professional advisers acting for persons involved in JFSC enforcement matters, and

- Other stakeholders with an interest in the JFSC enforcement framework and published methodology.

Summary of proposals

The proposed amendments would update the registered persons methodology to reflect

- The Financial Services Commission (Financial Penalties) (Jersey) Amendment Order 2026,

- Which reintroduced maximum penalties for Bands 1, 2 and 2A for registered persons, while Band 3 remains uncapped.

The JFSC are also proposing targeted updates to improve guidance in parts of the methodology, based on the JFSC experience of applying the regime in practice.

This consultation is limited to the methodology for registered persons.

Natural person

- The JFSC will consider the natural persons methodology separately at a later stage.

SOURCES

- Read the full consultation on amendments to the JFSC’s civil financial penalty methodology for registered persons.

- https://www.jerseyfsc.org/industry/consultations/consultation-on-amendments-to-the-jfsc-s-civil-financial-penalty-methodology-for-registered-persons/

- View the proposed revised methodology at Appendix A.

- https://www.jerseyfsc.org/media/3dggzdys/civil-fin-penalties-rp-metholology-final-draft-march-2026.pdf

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.