Chief Compliance Officer and Deputy Fined and Suspended Before Canaccord's $120M AML Penalty

17/05/2026

In early 2026, FinCEN, the SEC, and FINRA coordinated one of the largest anti-money laundering (AML) enforcement actions in U.S. broker-dealer history,

- Imposing combined penalties exceeding $120 million on Canaccord Genuity LLC

- For systemic and wilful Bank Secrecy Act (BSA) violations spanning more than a decade. (see separate story below)

Chief Compliance Officer and Deputy Fined and Suspended

- Before the 2026 firm-level penalties,

- FINRA had already taken individual enforcement action in 2025 against two senior compliance executives at Canaccord for their personal responsibility in the firm's prolonged AML failures.

- The sanctions

- Were issued on June 16, 2025, and

- Cover the period from 2017 through 2022.

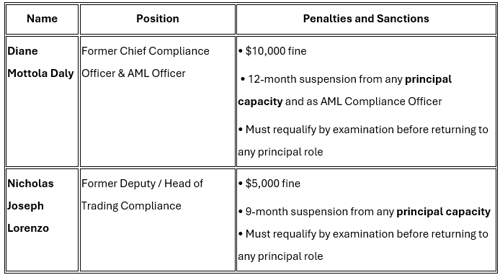

Sanctioned Individuals

Why the Compliance Officers Were Sanctioned

What significantly compounded the case's severity was Canaccord's prolonged awareness of serious AML deficiencies, coupled with years of inaction.

FINRA had repeatedly warned the firm about weaknesses in its AML program as early as 2014, and again in 2017 and 2018.

These warnings specifically flagged the urgent need for:

- Automated AML trade surveillance (due to high market-making volumes)

- Improved review of suspicious trading activity

- Timely follow-up on surveillance outputs

Despite providing written commitments to fix these issues, meaningful corrective action was delayed for years. According to FinCEN, significant remediation efforts began only after regulators launched their formal investigation.

At the compliance function level, the internal failures were particularly egregious.

- Surveillance reports were unreviewed for as long as 4 years, directly preventing the filing of hundreds of required Suspicious Activity Reports (SARs) with FinCEN.

- Furthermore, the firm's annual independent AML audits failed to identify or address the elevated risks inherent in its OTC and low-priced securities business lines.

In response to these serious lapses, FINRA sanctioned two senior compliance executives for failing to implement and maintain an effective AML compliance program.

Key Findings

- Diane Daly

- Failed to supervise the firm's AML transaction surveillance program reasonably and allowed surveillance reports to go completely unreviewed for periods of up to four years.

- This directly resulted in hundreds of suspicious activities going uninvestigated or unreported via SARs.

- Nicholas Lorenzo

- Failed to ensure that delegated surveillance reviews were actually being performed and ignored clear red flags that the monitoring process had broken down.

- Both individuals accepted the findings through FINRA's Letter of Acceptance, Waiver, and Consent (AWC) without admitting or denying the allegations.

Significance

- These personal sanctions reinforce a growing regulatory trend:

- Compliance leaders can and will be held individually accountable for systemic AML program failures even in the absence of personal financial gain.

- The action sends a strong message that:-

- "Paper compliance" programs,

- Chronic under-resourcing, and

- Failure to act on known deficiencies carries personal liability risks, including:-

- Fines,

- Suspensions, and

- Career-altering requalification requirements.

Primary Official Sources

- FinCEN Consent Order & Press Release https://www.fincen.gov/news/news-releases/fincen-assesses-historic-80-million-penalty-against-canaccord-genuity-llc https://www.fincen.gov/system/files/2026-03/Canaccord-Consent-Order-No-2026-01.pdf

- SEC Order https://www.sec.gov/files/litigation/admin/2026/34-104935.pdf https://www.sec.gov/enforcement-litigation/administrative-proceedings/34-104935-s

- FINRA Firm Penalty (related announcements) Various law firm and news summaries reference the $20M FINRA penalty as part of the coordinated action.

Individual Sanctions (Diane Daly & Nicholas Lorenzo)

- Radical Compliance – FINRA Sanctions Two Compliance Officers https://www.radicalcompliance.com/2025/06/19/finra-sanctions-two-compliance-officers/

- Law360 – FINRA Fines Ex-Canaccord Compliance Head https://www.law360.com/articles/2354623/finra-fines-ex-canaccord-compliance-head-over-monitoring

- FINRA BrokerCheck – Diane Mottola Daly https://brokercheck.finra.org/individual/summary/2372551

- FINRA BrokerCheck – Nicholas Joseph Lorenzo https://brokercheck.finra.org/individual/summary/2630518

Additional In-Depth Analysis & Summaries

- Foreign Policy Journal – Record-Breaking AML Fine https://www.foreignpolicyjournal.com/2026/05/16/record-breaking-aml-fine-against-canaccord-genuity-sends-warning-across-us-broker-dealer-industry/

- Paul, Weiss Client Memo https://www.paulweiss.com/insights/client-memos/fincen-the-sec-and-finra-assess-an-80-million-penalty-against-a-broker-dealer-for-anti-money-laundering-failures

- JD Supra – McDermott Will & Schulte https://www.jdsupra.com/legalnews/fincen-imposes-record-80-million-5217395/

- Chapman and Cutler LLP https://www.chapman.com/publication-fincen-imposes-80-million-civil-money-penalty-on-canaccord-genuity-llc-for-willful-violations-of-the-bank-secrecy-act-its-largest-fine-ever-against-a-broker-dealer

These links cover the full story: the $120M+ coordinated penalties, the $80M FinCEN record fine, and the personal sanctions against Diane Daly and Nicholas Lorenzo.

SUPPORTING STORY-

$120 Million Wake-Up Call: How Canaccord's Epic AML Failure Just Rewrote the Rules for Wall Street

Executive Summary: Record $120M+ AML Enforcement Action Against Canaccord Genuity LLC (March 2026)

In early 2026, FinCEN, the SEC, and FINRA coordinated one of the most significant anti-money laundering (AML) enforcement actions in U.S. broker-dealer history.

SYSTEMIC AND WILFUL BANK SECRECY ACT (BSA) VIOLATIONS

- Canaccord Genuity LLC, a Canadian-owned firm, faced combined penalties exceeding $120 million for SYSTEMIC AND WILFUL BANK SECRECY ACT (BSA) VIOLATIONS spanning more than a decade.

FinCEN SEC IMRA imposed fines:-

- An $80 million civil money penalty (the largest ever against a broker-dealer),

- With the SEC and FINRA each adding $20 million penalties (credited toward the total).

- An additional $5 million of the FinCEN penalty was suspended pending a satisfactory suspicious activity lookback review.

Canaccord's Chief Compliance Officer and her deputy were sanctioned.

- FINRA separately sanctioned the former Chief Compliance Officer and her deputy.

The firm admitted to three core violations:

- Failing to develop, implement, and maintain an effective AML program.

- Inadequate due diligence on correspondent accounts for foreign financial institutions.

- Failing to file at least 160 suspicious activity reports (SARs) related to thousands of suspicious transactions in dozens of over-the-counter (OTC) low-priced securities.

Conduit For Securities Fraud Schemes

These deficiencies enabled the firm to serve as a conduit for securities fraud schemes, including.

- Pump-and-dump and market manipulation activities that harmed investors.

Key structural failures included

- Chronic under-resourcing of the AML program,

- Insufficient monitoring and staffing relative to high-risk business lines,

- Unreviewed surveillance reports (for up to four years),

- Inadequate training and controls, and delayed remediation despite repeated FINRA warnings in 2014, 2017, and 2018.

- Annual independent AML audits also failed to identify risks.

This action shows a shift toward coordinated, high-impact enforcement focused on actual risk exposure rather than just technical compliance.

Global Compliance Warning

- This landmark case serves as a stark wake-up call to all broker-dealers, market makers, and clearing firms worldwide that interact with U.S. markets or handle cross-border flows.

- Regulators will no longer tolerate AML programs that are misaligned with business risk profiles—particularly in high-risk OTC/low-priced equity trading.

- Prior regulatory warnings, deferred remediation, unreviewed alerts, and under-resourced compliance functions are now viewed as wilful violations carrying severe civil, criminal, and individual liability risks.

- The coordinated FinCEN-SEC-FINRA approach, combined with the 2026 National Money Laundering Risk Assessment, signals heightened scrutiny and enforcement alignment. Firms ignoring these lessons risk multi-agency actions, massive fines, reputational damage, and personal sanctions for compliance leadership. The era of deferred remediation has ended.

Prevention Action List

Broker-dealers should immediately implement or strengthen the following measures to mitigate exposure:

- Business Risk Assessment:

- Conduct comprehensive, documented, and ongoing assessments of all business lines, products, services, and distribution channels (especially OTC/low-priced securities and market-making) to identify and quantify inherent AML risks accurately.

- Customer Risk Assessment:

- Implement robust, risk-based customer due diligence (CDD) and customer risk rating processes, with enhanced ongoing monitoring for high-risk customers, politically exposed persons (PEPs), and those with connections to illicit actors.

- Risk-Based AML Program Overhaul:

- Ensure the AML program is fully resourced, documented, and proportionate to the firm's business model and identified risks, with particular focus on OTC/low-priced securities, market-making volumes, and correspondent accounts.

- Automated Surveillance Implementation:

- Deploy and maintain robust automated trade surveillance systems capable of handling transaction volumes, with timely review protocols to prevent backlogs (e.g., no multi-year unreviewed reports).

- Enhanced Due Diligence (EDD):

- Conduct rigorous, ongoing due diligence on high-risk customers, foreign financial institutions, and correspondent relationships.

- SAR Filing Discipline:

- Establish clear triggers, escalation paths, and accountability for timely SAR filings on suspicious activity.

- Remediation and Testing:

- Respond promptly and substantively to all regulatory findings; conduct thorough independent AML audits that accurately reflect business risks; perform regular lookback reviews.

- Training and Governance:

- Provide role-specific AML training and ensure compliance leadership has adequate authority, resources, and accountability.

- Documentation and Accountability:

- Maintain comprehensive records demonstrating effective implementation; assign clear ownership to prevent "paper programs."

- Board and Senior Management Oversight:

- Ensure active engagement and periodic reporting on AML effectiveness relative to evolving risks.

Firms should treat the Canaccord consent order as a compliance benchmark and proactively benchmark their programs against it to avoid similar enforcement outcomes.

LONG READ

The US financial crime enforcement landscape shifted significantly in early 2026 when three regulators coordinated to deliver what has become the most consequential anti-money laundering action against a broker-dealer in American history.

The Financial Crimes Enforcement Network, the Securities and Exchange Commission, and the Financial Industry Regulatory Authority jointly sanctioned Canaccord Genuity LLC, a Canadian-owned broker-dealer operating across US markets, with combined penalties totalling more than $120 million for systemic and wilful failures under the Bank Secrecy Act spanning more than a decade.

FinCEN's portion of the action, an $80 million civil money penalty issued on 6 March 2026, represents the largest penalty ever imposed against a broker-dealer for Bank Secrecy Act violations. The SEC and FINRA each assessed penalties of $20 million, and FinCEN credited Canaccord’s payment of those amounts against the total. Of the $80 million owed to FinCEN, $5 million was suspended pending the successful delivery of a satisfactory suspicious activity lookback review pursuant to the terms of the consent order.

The substance of the enforcement action is damning by any measure. Canaccord admitted wilfully violating the Bank Secrecy Act on three core fronts: failing to develop, implement, and maintain an effective anti-money laundering programme; failing to conduct required due diligence on correspondent accounts for foreign financial institutions; and failing to file suspicious activity reports when required by law. FinCEN's findings documented that the firm failed to file at least 160 suspicious activity reports relating to dozens of different over-the-counter securities, with underlying suspicious transactions estimated to be in the thousands.

Those failures enabled the firm to serve as a conduit for securities fraud schemes that caused significant economic harm to investors and facilitated the onboarding of high-risk customers with reported connections to illicit actors.

The structural nature of the failure is what makes the Canaccord case particularly instructive for the broader broker-dealer community. FinCEN found that Canaccord's anti-money laundering programme was materially under-resourced and that its monitoring procedures, staffing, training, and internal controls were not proportionate to the risks generated by its business model. The firm was heavily involved in low-priced equity transactions across over-the-counter markets, an environment historically associated with elevated fraud risk including pump-and-dump schemes and market manipulation. Despite operating in that space, the firm’s surveillance infrastructure failed to keep pace with the volume and nature of the activity.

What compounded the severity of the regulatory findings was the timeline of awareness and inaction. FINRA had warned Canaccord about aspects of its AML programme in 2014, 2017, and 2018, flagging deficiencies including the need for automated AML trade surveillance given the firm’s market-making volumes, the need to improve review of suspicious trading activity, and the need to ensure timely review of surveillance outputs. Despite written commitments to remediate those weaknesses, meaningful corrective action was not taken for years. According to FinCEN, significant aspects of the firm’s remediation programme were not undertaken until the regulator’s investigation was already underway.

Further detail emerged regarding internal conduct at the compliance function level. Surveillance reports went unreviewed for as long as four years, directly suppressing the volume of suspicious activity reports being filed with FinCEN. The firm’s annual independent AML audits were found to reflect an inadequate understanding of the risks inherent in the relevant business lines, meaning the external assurance mechanism that should have caught the dysfunction was itself compromised. FINRA separately sanctioned Diane Daly, Canaccord’s former chief compliance officer, and Nicholas Lorenzo, her former deputy who managed the trading compliance group, for failing to implement an effective AML compliance programme across the period from 2017 through 2022.

FinCEN Director Andrea Gacki framed the action as a wake-up call to broker-dealers that wilfully fail to comply with their obligations to safeguard the financial system from illicit actors. That framing is significant in the context of the current regulatory environment. Under SEC chair Paul Atkins, the Commission has adopted an enforcement posture described as enforcement for impact, concentrating resources on misconduct that causes the greatest harm to investors. The Canaccord action fits that framework precisely, combining securities fraud exposure with AML failures in a manner that caused documented harm to retail market participants.

The implications for broker-dealers operating in similar business lines are substantial. Firms engaged in market-making or clearing for low-priced OTC securities must now reckon with the fact that FinCEN and FINRA will assess their AML programmes not merely against technical compliance checklists but against the actual risk profile of the business. Inadequate staffing, unreviewed surveillance outputs, and deferred remediation will not be treated as administrative shortcomings. The Canaccord resolution makes clear they constitute wilful violations with criminal and civil consequences. Compliance officers at firms including Virtu Financial, Citadel Securities, and other active participants in OTC markets will be reviewing their programmes in light of the specific deficiencies cited across the 13-year failure period identified in the consent order.

The coordinated nature of the action itself signals increasing alignment between FinCEN, the SEC, and FINRA on AML enforcement in securities markets, an area where historically the three agencies have operated with limited joint visibility. The 2026 National Money Laundering Risk Assessment published by the US Treasury explicitly acknowledged that broker-dealers face exposure from customers seeking to disguise illicit proceeds within legitimate trades or engage in fraudulent trading activity involving low-priced securities. That assessment now has direct enforcement precedent attached to it.

For compliance functions across US-registered broker-dealers, the Canaccord case introduces a practical benchmark: AML programmes that cannot demonstrate adequate resourcing, automated surveillance appropriate to business volumes, timely review processes, and meaningful responses to prior regulatory findings are now structurally exposed to enforcement actions that follow the same coordinated model. The era of deferred remediation has ended.

SOURCES

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.