ASK MAT – JCOA Sanctions Event: Should the JFSC Update Its Three-Tier Test for Beneficial Ownership and Controllers?

17/04/2026

ASK MAT – JCOA Sanctions Event: Should the JFSC Update Its Three-Tier Test for Beneficial Ownership and Controllers?

I'm asking this question because, in a recent JCOA Sanctions Event, Collingwood Thompson KC highlighted several sanction risks in a presentation titled.

- “Legal Issues in Control- Between a Rock and a Hard Place”

Some of these issues were

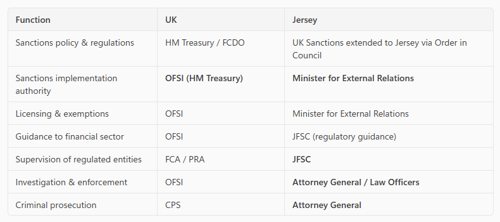

- JERSEY SANCTIONS FRAMEWORK:

- Missteps in Jersey sanctions compliance can result in serious criminal liability, including fines and imprisonment of up to seven years.

- NOTE: -Unlike the UK, Jersey does not operate a standalone OFSI‑style civil monetary penalty regime, meaning enforcement is primarily criminal rather than administrative.

- THE LEGAL RISK IN JERSEY BEING

- “Jersey sanctions are governed by the Sanctions and Asset‑Freezing (Jersey) Law 2019, with UK and other external sanctions regimes implemented locally through the Sanctions and Asset‑Freezing (Implementation of External Sanctions) (Jersey) Order 2021.”

- SEE APPENDIX 1

- CONTROL DEFINITIONS:

- Legal definitions of control extend beyond ownership; hypothetical influence also plays a significant role.

- COMSURE NOTES FROM THE TALK ARE HERE

MAT SAYS:

- Thank you for your question.

- In short, yes. I made this exact point on 18 February 2026 in another ASK MAT article on the Comsure news site:

- “ASK MAT – Do you think the JFSC should revisit and update its three-tier test for beneficial ownership and controllers?”

[Read the full article on comsuregroup.com]

Why this matters (the Comsure position)

- Jersey firms are supervised using a three-tier AML-derived framework, yet the same firms are legally exposed to a four-tier UK sanctions test.

- This mismatch creates:

- False assurance from AML reviews

- Sanctions misclassification risk

- Tension between Jersey and UK sanctions regulators, such as the OFSI, HMRC, FCA/PRA, the JFSC, and the Jersey Government

- Comsure’s view is clear: the JFSC should explicitly modernise its guidance to reflect the UK sanctions reality, particularly the concept of hypothetical control.

Summary of the February 2026 ASK MAT

- The February article built on material presented in a Comsure sanctions briefing.

- It highlighted growing concern that Jersey’s existing three-tier test for identifying beneficial owners and controllers is now out of step with UK sanctions law and recent case-law developments.

What is the “three-tier test” in a Jersey context?

- Under JFSC guidance, firms typically assess control through a structured three-tier approach:

- Legal ownership (usually >50% shareholding or voting rights)

- Board control (right to appoint or remove directors)

- Other means of control (e.g. veto rights, shareholder agreements)

- This framework works well for AML/CFT beneficial ownership purposes, but it was never designed for modern sanctions typologies, especially those involving structured influence, proxy arrangements, and geopolitical actors.

Why sanctions have changed the game

- Since 2022, UK sanctions, particularly under the Russia (Sanctions) (EU Exit) Regulations 2019, have significantly expanded the interpretation of “control”.

- The UK Office of Financial Sanctions Implementation (OFSI) has publicly acknowledged that Regulation 7’s ownership and control test lacks clarity and proportionality.

- Firms are now expected to assess hypothetical control, i.e. what a sanctioned person could do, not just what they are doing.

- This goes well beyond traditional [3-tier] beneficial ownership analysis.

The impact of recent UK case law

- UK courts have effectively refined the control test, creating what now looks like a four-tier typology.

- Cases such as Vneshprombank v Bedzhamov (and others examined by UK Finance and leading law firms) confirm that:

- Control can exist without ownership

- Influence may be informal, indirect, or situation-dependent

- Courts focus on real-world ability to influence outcomes, not just formal documents

- This judicial approach is feeding directly into regulatory expectations.

Why Comsure believes the JFSC should amend its approach

- Jersey firms must comply with UK sanctions, yet they are assessed by the JFSC using older AML-era control concepts.

- This creates:

- Supervisory risk (firms pass JFSC tests but fail THE expectations OF OFSI, HMRC, FCA/PRA, and Jersey Government

- Legal risk (incorrect sanctions determinations)

- Operational uncertainty for boards and compliance officers

- Comsure therefore argues that the JFSC should update its three-tier test to explicitly incorporate the UK’s emerging four-tier sanctions typology, especially around hypothetical and situational control.

Timing is critical: OFSI’s Call for Evidence

- OFSI opened a formal Call for Evidence on the ownership and control test in February 2026 (closed 13 April 2026).

- Comsure’s article deliberately aligned the Jersey discussion with this process, signalling that change is coming at the UK level and that Crown Dependencies will be expected to keep pace.

What this means in practice for Jersey firms

- If the JFSC amends its approach (as Comsure recommends):

- Sanctions assessments will need to go beyond ownership charts

- Firms may need to document why hypothetical control is rejected

- Boards will require clearer risk-based reasoning rather than binary tests

- Outsourcing, fiduciary, and fund structures will face greater scrutiny

This has direct implications for compliance frameworks, risk assessments, and training, especially for firms with exposure to politically sensitive jurisdictions.

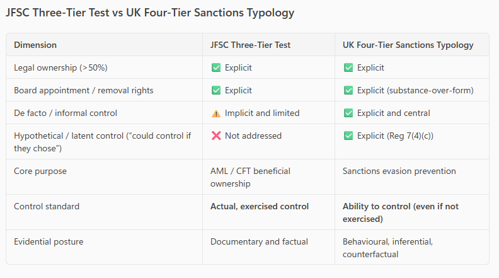

PART 2: Mapping – JFSC Three-Tier Test vs UK Four-Tier Sanctions Typology

- Tier 1 – Legal / Majority Ownership JFSC (Three-Tier Test):

- Focuses on legal ownership (>50% shares or voting rights) based on share registers and formal legal title (AML/CFT concepts).

- UK Sanctions (Tier 1): Identical 50% threshold under Regulation 7 (direct or indirect).

- Assessment: ✅ Fully aligned – no material regulatory gap.

- Tier 2 – Board Control / Appointment Rights JFSC:

- Right to appoint or remove directors, evidenced by constitutional documents and formal agreements.

- UK Sanctions (Tier 2): Same legal limb but applied substantively; nominee/proxy arrangements, reserved matters and indirect powers are scrutinised (substance over form).

- Assessment: ⚠️ Conceptually aligned, but the UK applies a more forensic analysis.

- Tier 3 – De facto / “Other Means” of Control JFSC:

- Covers veto rights, contractual leverage, etc., but typically requires actual, demonstrable exercise of control.

- UK Sanctions (Tier 3): Explicit recognition of de facto and informal control; repeated or decisive influence can be sufficient.

- Assessment: ⚠️ Superficially similar, but the UK approach is broader and more intrusive.

- Tier 4 – Hypothetical / Situational Control JFSC Position:

- No express provision; control is assessed only where exercised (AML-centric).

- UK Sanctions (Tier 4): Control exists where it is reasonable to expect a designated person could control if they chose to (in most cases or significant respects). Focus on ability and situational power.

- Assessment: ❌ No JFSC equivalent – this is the principal regulatory and compliance gap for Jersey firms.

PART 3: Suggested Policy Insert – Sanctions Control Assessment (Additional Considerations)

- Here is ready-to-use policy language that acknowledges UK sanctions expectations without overstating Jersey supervisory requirements. It recognises Tier 4 without importing it wholesale into the JFSC three-tier test.

Suggested Guidance / Policy Insert

Sanctions Control Assessment – Additional Considerations

In applying the Jersey three-tier test for beneficial ownership and control, the Firm recognises that, in the context of UK financial sanctions, overseas authorities may apply a broader interpretation of “control”.

This includes circumstances in which an individual may reasonably be considered capable of exerting decisive influence, even if that influence is not actively exercised.

Accordingly, where sanctions exposure is identified, the Firm will:

- Perform a documented assessment of actual control in line with JFSC guidance; and

- Record its consideration of whether any individual may plausibly be able to exert control, having regard to governance, economic dependency, personal influence, or situational leverage.

The Firm does not treat potential or hypothetical influence as determinative of control for Jersey regulatory purposes. However, where such factors are identified, they are assessed as part of sanctions risk management and escalated where appropriate.

This approach ensures alignment with UK sanctions obligations while remaining consistent with Jersey regulatory expectations.

Why this policy works

- ✅ Acknowledges the sanctions Tier 4 concept

- ✅ Avoids importing counterfactual control as a legal test for the JFSC three-tier test

- ✅ Demonstrates regulatory awareness and proportionality

APPENDIX 1 - You cannot have SAFO without SAFL.

SAFL (Jersey) OR “the Jersey sanctions law”.

Sanctions and Asset‑Freezing (Jersey) Law 2019

- This is the primary sanctions law in Jersey.

- It provides the legal framework that allows UK, UN, and other international sanctions regimes to be given effect in Jersey.

- It establishes:

- Sanctions offences

- Asset‑freezing powers

- Licensing powers

- Enforcement and investigation powers

- It designates the Minister for External Relations as the competent authority for sanctions.

SAFO (Jersey) OR “the sanctions Order”.

Sanctions and Asset‑Freezing (Implementation of External Sanctions) (Jersey) Order 2021

- This is the principal implementing Order made under SAFL.

- It is the mechanism by which:

- UK sanctions regulations (e.g. Russia, Iran, counter‑terrorism)

- UN sanctions are applied in Jersey.

- Each time the UK updates or introduces a sanctions regime, it is typically:

- Extended to Jersey via this Order (and amendments to it)

How they work together (plain English)

- SAFL = the enabling legislation (the legal engine)

- SAFO = the implementation mechanism (the gearbox that brings UK sanctions into Jersey)

- You cannot have SAFO without SAFL.

Sources

- www.comsuregroup.com/news/ask-mat-do-you-think-the-jfsc-should-revisit-and-update-its-three-tier-test-for-beneficial-ownership-and-controllers/

- www.comsuregroup.com/news/decoding-the-uks-sanction-ownership-and-control-test-challenges-hypotheticals-and-the-push-for-reform/

- www.gov.uk/government/calls-for-evidence/ownership-and-control-test-in-uk-financial-sanctions-regulations/ownership-and-control-test-in-uk-financial-sanctions-regulations

- www.gov.uk/government/publications/ownership-and-control-test-in-uk-financial-sanctions-regulations-call-for-evidence

- www.skadden.com/insights/publications/2024/09/control-under-the-uks-sanctions

- www.ukfinance.org.uk/news-and-insight/blog/recent-developments-in-sanctions-case-law-england-and-wales

- https://www.comsuregroup.com/news/ask-mat-do-you-think-the-jfsc-should-revisit-and-update-its-three-tier-test-for-beneficial-ownership-and-controllers/

- https://www.ukfinance.org.uk/news-and-insight/blog/recent-developments-in-sanctions-case-law-england-and-wales

- https://www.skadden.com/insights/publications/2024/09/control-under-the-uks-sanctions

- https://www.gov.uk/government/calls-for-evidence/ownership-and-control-test-in-uk-financial-sanctions-regulations/ownership-and-control-test-in-uk-financial-sanctions-regulations

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.