ASK MAT I’m a Jersey-regulated person, and my client is SELLING a house. What CDD do I need on the BUYER, if any?

30/04/2026

ASK MAT I’m a Jersey-regulated person, and my client is SELLING a house. What CDD do I need on the BUYER, if any?

I’m asking because a lawyer at a conference said that:-

- Where a regulated person is acting for the seller of a property, the buyer is not subject to the CDD requirement (see the transcript in Appendix 1).

This concerned me:-

- My understanding was that, under the Money Laundering (Jersey) Order 2008 (MLO), where a person is involved in a one-off transaction, limited CDD must still be applied based on a risk assessment.

At a minimum, I understood that:-

- Under the MLO, I must carry out identification measures and a risk assessment; and

- The JFSC AML/CFT/CPF Handbook, in the estate agency sector, states that both buyers and sellers must be subject to CDD.

My question is:-

- Is it, therefore, correct to say that the buyer of the house IS NOT a CDD subject under the MLO?

MAT’S ANSWER

Mat says

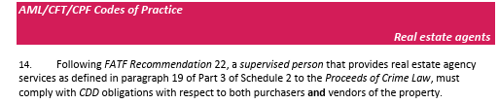

- What a great question, thank you for raising it.

- One-off transactions in property deals continue to receive attention from both regulated persons and the regulator.

- I’m sure that, should anything go wrong, the matter will be analysed in considerable depth.

- I’m pleased this issue has been aired publicly.

- The lawyer at the conference gave an answer I can largely agree with in the specific context he was addressing.

- He was speaking about a regulated business acting as trustee (i.e. a regulated Trust Company Business (TCB) / regulated trustee) and its customer.

- In that scenario, his analysis holds good

- But, as this response shows, the correct position still depends heavily on the exact regulated activity you are carrying out.

- It would have been helpful if the speaker had asked the questioner to confirm their precise role (e.g., estate agent),

- Although I understand that the conference was for TCB operators, I understand why he did not ask

MATS ANSWER

- As you do not tell me your activity, are you a TCB, an estate agent or another? Therefore, my short answer is:

- It depends entirely on your role in the transaction.

- Therefore, my conclusion is that the conference speaker was

- Correct in one scenario,

- But incorrect in the other.

- The confusion arises when the two situations are conflated.

HERE ARE TWO SCENARIOS

- IF YOU ARE PROVIDING ESTATE AGENCY SERVICES (I.E., YOU ARE THE REGULATED ESTATE AGENT)

YES, THE BUYER IS A CDD SUBJECT.

- Where you carry on estate agency services as a supervised person, both the buyer (purchaser) and the seller (vendor) are your customers for AML purposes.

- You must apply CDD measures to both. This requirement is mandatory.

LEGAL BASIS

- A typical property sale through an estate agent is a one-off transaction (not a business relationship) within the meaning of Article 4 of the MLO.

- Article 13(1)(b) of the MLO requires CDD measures to be applied before carrying out a one-off transaction.

- Article 3 of the MLO defines “customer due diligence measures” as including identification measures, obtaining information on the purpose and intended nature of the transaction, a money-laundering risk assessment, and (where relevant) ongoing monitoring.

SECTOR-SPECIFIC RULES

- Section 14 of the JFSC AML/CFT/CPF Handbook (Estate Agents and High Value Dealers) explicitly requires estate agents to treat both vendors and purchasers as customers and to apply CDD to each of them, even in one-off transactions.

- These Handbook rules are binding AML/CFT Codes of Practice.

WHAT CDD ACTUALLY REQUIRES IN A ONE-OFF PROPERTY SALE.

In a low-risk one-off transaction, the minimum identification measures are:

- Identifying the buyer;

- Understanding the purpose and intended nature of the transaction;

- Carrying out and recording a transaction-specific ML risk assessment.

- Verification of identity (obtaining documentary evidence) is risk-based only (Article 3(6) MLO — measures must be reasonable and proportionate to the assessed risk).

ARTICLE 18(6) EXEMPTION (JERSEY PROPERTY CONTRACTS).

- Where the transaction involves a Jersey property contract passed before the Royal Court and registered in the Public Registry, Article 18(6) of the MLO provides an exemption from obtaining evidence of identity (verification).

Important:

- This exemption is available only in respect of your own customer.

- As a regulated estate agent, both the buyer (purchaser) and the seller (vendor) are your customers, so the exemption can be applied to the buyer (and the seller), allowing you to dispense with verification of identity, provided you:

- Still identify the customer; and

- Retain documentation showing that the exemption applies.

- This is why, in standard low-risk Jersey residential sales, buyers often require only identification + risk assessment rather than full documentary verification (e.g. passport + utility bill).

- Higher-risk cases still require verification and, where appropriate, enhanced due diligence (source of funds/wealth).

BOTTOM LINE FOR ESTATE AGENTS

- The buyer is a CDD subject.

- One-off status limits the depth of CDD but does not remove the obligation.

- The Handbook requirement is clear, mandatory, and takes precedence.

- IF YOU ARE A REGULATED PERSON ACTING ONLY FOR THE SELLER AND YOU ARE NOT PROVIDING ESTATE AGENCY SERVICES (E.G., A REGULATED TRUST COMPANY BUSINESS (TCB) ACTING AS TRUSTEE, A LAWYER/ADVOCATE HANDLING CONVEYANCING, OR SIMILAR)

NO, THE BUYER ISN'T A CDD SUBJECT FOR YOU.

- This is precisely the scenario the conference speaker addressed (a regulated trustee/TCB and its customer).

- His analysis is correct here.

- Your customer is the seller. The buyer is a third-party counterparty.

- Receiving purchase money into your client account does not, by itself, create a business relationship or a separate one-off transaction with the buyer under the MLO.

WHAT YOU MUST STILL DO (RISK-BASED APPROACH) Although formal CDD is not required for the buyer, you cannot simply ignore them.

You must consider all risks associated with the seller, including the risk of receiving funds.

- Apply full CDD (identification, verification where required, risk assessment, source of funds/wealth) to your client, the seller;

- Understand the purpose and intended nature of the transaction;

- Carry out an overall transaction risk assessment;

- Consider source of funds risk:- consider proceeds of crime, terrorist funds, proliferation exposure, along with sanction issues

- Take reasonable, proportionate steps regarding the buyer and incoming funds, such as:

- Name screening;

- Taking comfort from the buyer being represented by a reputable advocate/solicitor (risk assessment);

- For example, are funds coming through a

- Lawyer’s client account or

- Mainstream banking channels;

- document your risk assessment and decisions;

ARTICLE 18(6) EXEMPTION (JERSEY PROPERTY CONTRACTS)

- Where the transaction involves a Jersey property contract passed before the Royal Court and registered in the Public Registry, Article 18(6) of the MLO provides an exemption from obtaining evidence of identity (verification).

- This exemption is available only in respect of your own customer (the seller). It allows you to dispense with verification of the seller, provided you:

- Still identify the seller; and

- Retain documentation showing that the exemption applies.

- Because you are acting only for the seller in this scenario, Article 18(6) does not apply to the buyer (who is a third-party counterparty, not your customer).

SUMMARY

SARS

- IN BOTH CASES, if there is a red flag, submit a Suspicious Activity Report (SAR) promptly to

- The JFIU [PolSAR] if suspicion of MONEY LAUNDERING OR TERRORIST FINANCING arises (Proceeds of Crime (Jersey) Law 1999); and

- the Minister for External Relations, ANY SANCTIONS MATCH, FROZEN ASSETS, OR SUSPECTED SANCTIONS BREACH (using the Sanctions Compliance Reporting Form sent to sanctions@gov.je), as required under Article 32 of the Sanctions and Asset-Freezing (Jersey) Law 2019 (this obligation is separate from and in addition to any FIU SAR);

CONCLUSION

- The statement

- “The buyer is not a CDD subject” is incorrect for regulated estate agents

- But correct for professionals acting solely for the seller (including regulated TCBs / trustees).

- The one-off transaction concept limits the extent of CDD; it does not eliminate it where the JFSC Handbook imposes a sector-specific obligation.

- The Handbook position is authoritative and binding on supervised persons.

If you are in any doubt, speak to your MLRO or Comsure, or the lawyer from the conference and/or seek specific confirmation from the JFSC.

KEY SOURCES

- Money Laundering (Jersey) Order 2008 (as amended – current version): https://www.jerseylaw.je/laws/current/ro_20_2008

- Proceeds of Crime (Jersey) Law 1999 (as amended): https://www.jerseylaw.je/laws/current/l_8_1999

- JFSC AML/CFT/CPF Handbook – Section 14: Estate Agents and High Value Dealers (clean version): https://www.jerseyfsc.org/media/7029/handbook-section-14-clean.pdf

- JFSC AML/CFT/CPF Handbook – Section 15: Lawyers (clean version): https://www.jerseyfsc.org/media/7030/handbook-section-15-clean.pdf

- JFSC AML/CFT/CPF Handbook main page (all sectors, including 2026 updates): https://www.jerseyfsc.org/industry/financial-crime/amlcftcpf-handbooks/amlcftcpf-handbook/

Appendix 1

TRANSCRIPT = THIS IS WHAT THE SPEAKER SAID (as I recorded them – my best endeavours)

SPEAKERS SAYS:-

- “To third parties, using terms of art in the way the money laundering order intended. Well, one-off transactions are another example of that. The phrase ‘one-off transaction’ is used in contrast to the phrase ‘business relationship’.

- That explains the duration of the interaction among the regulated business, the trustee, the regulated trustee, and the regulated trustee's customer.

- It could be a business relationship, ongoing for X duration, or a one-off transaction, and that's that. But it describes the length or duration of the relationship between the regulated business and the customer.

So far, so good.

- The purchaser is not a customer.

- Are there any other labels that we can put on the purchaser?

- Third party? No. Wrong.

- For the reasons I spoke about before. Beneficial owner or controller? No. Wrong.

- Agent? No. Wrong.

- Not a CDD subject.

Does this fit within the process? No, it doesn't, because the purchaser is not a CDD subject.

This may leave some people dissatisfied, perhaps displeased, and sad. If the purchaser isn't a CDD subject, what should we do?

You still need to take action, because that's not an invitation to receive criminal property from someone simply because they're not a CDD subject.

Please take action; there's a risk you may breach criminal law.

Criminal law prohibits dealing in criminal property. And, this bloke, this purchaser, he might well be wrong. So what do you need to do?

Well, the answer isn't CDD.

That's completely wrong because he's not a CDD subject.

But you might do other things.

For example, please obtain his name and run a background check. To screen it properly, maybe you will need his passport.

That's different from accepting that you need his passport. If you accept that and take that position, you'll create a problem.

When he says, ‘I'm not giving you my passport,’ you might also look at who he's instructed.

Because, particularly, property transactions of the value that we're talking about, there'll be solicitors on board, and if it is a big city firm LLP that is acting for him, you can take a measure of comfort from that. If the money is coming from Big City Firm Solicitor LLP's trust account and is going through legitimate banks A to B, you could take some comfort in that.

You're responsible for the scope and the steps you take.

That's one of the very limited instances, and the risk-based approach you can take is quite limited. It is not a panacea. This doesn't address the risk-based approach.

Mate, I cringe when clients use that phrase unless they're using it correctly. In cases where someone isn't a CDD subject, take the necessary steps, assess the overall risk, and proceed accordingly.

The answer isn't to get a passport and get a utility bill, because when you're receiving money from somebody that isn't a CDD subject, that actually won't help you manage the risk at all.”

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.