ASK MAT: I am updating my Jersey EWRA[BRA] and have been told I need to read and apply the ISSB – what is this all about?

23/04/2026

ASK MAT: I am updating my Jersey EWRA[BRA] and have been told I need to read and apply the ISSB – what is this all about?

MAT SAYS: Thank you for an excellent question that im sure has slipped under the radar of many risk managers

- From 9 April 2026, the Jersey Financial Services Commission (JFSC) issued Sustainable Finance Guidance that applies to all registered persons.

- Crucially, the JFSC states that sustainability‑related risk assessments must be conducted using

- A single financial materiality lens aligned to the International Sustainability Standards Board (ISSB) framework.

- [ifrs.org] https://www.ifrs.org/sustainability/knowledge-hub/introduction-to-issb-and-ifrs-sustainability-disclosure-standards/

- “The ISSB operates under the IFRS Foundation and issues IFRS Sustainability Disclosure Standards (IFRS S1 and S2),

- This extends the IFRS framework to cover sustainability‑ and climate‑related risks that may affect an entity’s financial position, performance or prospects.”

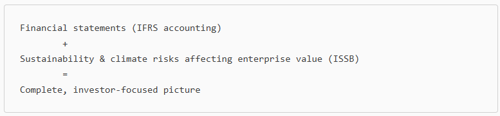

- How the two connect in practice

§ Traditional IFRS (IASB) - Answers:

- What are the entity’s assets, liabilities and profits?

- How are they measured and recognised?

§ ISSB (S1 & S2) Answers:

- What sustainability or climate risks could affect those assets, liabilities and profits in the future?

- What information do investors need to understand those risks?

- Together they create a single, coherent reporting system:

- This means:

- You ARE NOT required to adopt ESG “double materiality” (EU‑style impact reporting),

- But YOU ARE required to consider how sustainability risks affect your firm’s financial position, performance and prospects, exactly as defined by ISSB IFRS S1 and S2.

- In short:

- ISSB is now the conceptual backbone of Jersey’s sustainability risk expectations.

Below is a Jersey-specific, practical explanation of why the International Sustainability Standards Board (ISSB) matters for managing sustainability-related risks and what you need to do as a regulated firm or practitioner.

ISSB defines what counts as a “sustainability‑related risk” in regulatory terms

- The ISSB standards (IFRS S1 and S2) define sustainability‑related risks as risks that could reasonably be expected to affect enterprise value over the short, medium or long term.

- The JFSC adopts this same approach, meaning:

- Sustainability risk is not reputational fluff,

- It is a prudential, financial risk no different in principle from credit, liquidity or operational risk.

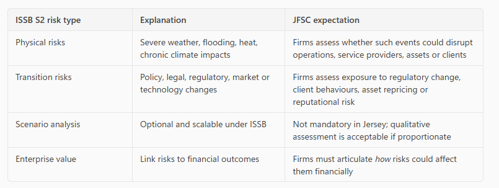

- This is why climate‑related (as shown below)must be considered within your core risk framework, not in a standalone ESG policy.

- Physical risks (e.g. flooding, heat stress affecting assets, funds, counterparties), and

- Transition risks (regulatory change, asset repricing, stranded assets, client exposures)

ISSB alignment protects Jersey’s international credibility

- Jersey’s Sustainable Finance Action Plan commits the Island to alignment with internationally recognised disclosure and risk standards, specifically ISSB, to:

- Maintain regulatory equivalence,

- Reduce greenwashing, and

- Ensure continued access to global capital markets.

- For firms, this means ISSB awareness is now part of being “fit and proper” in an international finance centre, not an optional extra.

What you need to do in practice (Jersey‑focused)

1. Integrate sustainability risks into your existing risk management framework

- The JFSC is clear:

- No new CODIFIED risk category is required.

- Instead, sustainability‑related risks are embedded into Principle 3 risk assessments under the Codes of Practice.

- You should be able to demonstrate:

- Identification of

- Material climate and

- Sustainability risks,

- Assessment of

- financial impact (not moral or societal impact),

- Integration into existing:

- Risk registers,

- Controls,

- Governance and escalation processes.

Notes on Alignment with ISSB S1 to help you decide what is financially material.

Notes on Alignment with ISSB S2 that provides the structure for climate‑specific risks.

2. Apply ISSB‑style financial materiality (not EU double materiality)

- The JFSC expressly states that:

- Only financial materiality is required,

- Impact‑on‑society assessments are optional.

- Practically, this means asking:

- Could climate or transition risks affect:

- Solvency?

- Liquidity?

- Asset values?

- Client demand?

- Operational continuity?

- This mirrors the ISSB definition of materiality under IFRS S1.

3. Ensure any sustainability‑related claims are defensible

- ISSB alignment feeds directly into Principle 7 (anti‑greenwashing).

- From 2026 guidance and into Q1 2027 enforcement, firms must ensure that any sustainability claim:

- Is fair, clear and not misleading,

- Can be evidenced by actual governance, data or processes.

- If you say you:

- “Manage climate risk”,

- “Consider ESG in investment decisions”,

- “Support sustainable finance”,

- you must be able to show ISSB‑consistent risk identification and oversight.

4. Prepare for supervisory scrutiny

- While Jersey does not mandate ISSB reporting, the JFSC may:

- Ask how you identified sustainability risks,

- Expect consistency with ISSB terminology and logic,

- Challenge firms whose risk assessments omit obvious climate or transition exposure.

- Being ISSB‑literate is therefore essential for:

- Desk‑based reviews,

- Thematic examinations,

- Onsite inspections.

In summary

- ISSB is not about reporting in Jersey — it is about risk thinking. The JFSC has anchored its sustainability risk expectations to ISSB concepts.

- You must:

- Identify sustainability‑related risks using financial materiality,

- Integrate them into existing risk frameworks,

- Avoid unsupported sustainability claims,

- Be able to explain your approach using ISSB‑consistent logic.

SOURCES

- JFSC – Sustainable Finance Guidance (Issued 9 April 2026)https://www.jerseyfsc.org/industry/guidance-and-policy/sustainable-finance/

- Comsure – Summary of JFSC Sustainability Risk Guidancehttps://www.comsuregroup.com/news/jfsc-new-guidance-effective-9426-requires-sustainability-related-risk-assessments-for-all-registered-persons/

- JFSC – Sustainable Finance Action Planhttps://www.jerseyfsc.org/industry/sustainable-finance/sustainable-finance-action-plan/

- Government of Jersey – Sustainable Finance Action Plan (2024)https://www.gov.je/SiteCollectionDocuments/Industry%20and%20finance/P%20Sustainable%20Finance%20Action%20Plan%202024.pdf

- IFRS / ISSB – Introduction to ISSB and IFRS S1 & S2https://www.ifrs.org/sustainability/knowledge-hub/introduction-to-issb-and-ifrs-sustainability-disclosure-standards/

- IFRS – ISSB Educational Material on Sustainability‑Related Risks

https://www.ifrs.org/content/dam/ifrs/supporting-implementation/issb-standards/issb-materiality-education-material.pdf

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.