A time to win? Is CRS compliance harder in Jersey? A change in March suggests that, for some, it is

31/03/2026

Revenue Jersey quietly released its updated CRS Technical Guidance Notes in March 2026. Buried on pages 17–19 is one of the clearest shifts in years: the “managed by” test for Type B Investment Entities has been hardened.

Jersey CRS Technical Guidance Notes (March 2026) https://www.gov.je/SiteCollectionDocuments/Tax%20and%20your%20money/Jersey%20CRS%20technical%20guidance%20March%202026.pdf

Where a regulated Jersey TCSP provides directors (or officers) and administers a Jersey company, that company “will be treated as being managed by a Financial Institution” even if the directors are appointed in an individual capacity, provided the contract sits with the TCSP. Also, meet the gross-income test, and the entity flips from Passive NFE (look-through to controlling persons) to full Financial Institution status.

For many private holding companies and family investment vehicles, this is not a minor clarification. It is a reclassification that requires additional due diligence, periodic reviews, upstream self-certification obligations, potential GIIN requirements, and direct reporting on equity/debt interests.

In other words: more compliance, more cost, more paperwork.

At the same time, the Jersey government is running its “A Time to Win” initiative, a high-profile drive to make the island more competitive by removing unnecessary regulation and red tape. The message has been consistent: Jersey wants to win business, not bury it in rules. [ https://www.gov.je/SiteCollectionDocuments/Government%20and%20administration/Time%20to%20Win%20report.pdf ]

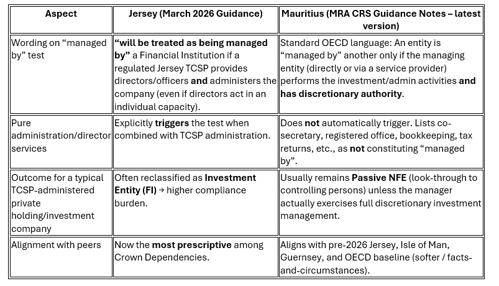

Yet this March CRS update does the opposite for a significant slice of TCSP-administered structures. While the Isle of Man and Guernsey still use the softer “may be treated as” language, Jersey has adopted the prescriptive “will be treated as”. Even more telling is the contrast with Mauritius. Following the March 2026 update, Mauritius has not followed Jersey’s tightening. Its latest CRS Guidance Notes still use the standard OECD facts-and-circumstances wording. Pure administration and director services provided by a Mauritius management company do not automatically trigger the “managed by” test. As a result, most private holding and family investment vehicles in Mauritius remain classified as Passive NFEs with a materially lower compliance burden than Jersey’s updated position.

This is not about ignoring global standards. Jersey must, and does, meet the OECD CRS. The issue is one of tone and timing. When your own government is publicly promising to cut regulatory friction to “win”, issuing tighter local guidance that increases friction feels inconsistent at best.

Certain clients will notice and ask questions.

Cost-sensitive family offices and private clients already weighing Jersey against Guernsey, the Isle of Man, Cayman, or now Mauritius will see this as another reason to pause. The industry has always accepted that robust compliance is the price of doing business here, but when the regulator tightens the screw. At the same time, the government talks about loosening it, the message to the market becomes mixed.

Revenue Jersey’s stated goal for the 2026 guidance was to “standardise application across the industry” and remove past ambiguity. That is understandable. But standardisation that makes Jersey materially stricter than its closest competitors (global IFCs) is not neutral; it has competitiveness consequences.

The March change may be technically correct under the CRS. The bigger question is whether it aligns with the “A Time to Win” rhetoric. For some structures, and for some clients, the answer right now appears to be no.

Jersey’s success has always rested on striking the right balance between reputation and practicality. This update tips the balance against a key segment of the market. If “A Time to Win” is to mean anything, future guidance and policy decisions need to reflect the same competitive mindset the government is asking the rest of us to adopt.

Below is a briefing paper on the changes and challenges

TCSP / TCB Board Briefing Paper Jersey CRS Technical Guidance Notes – March 2026 Update Focus: Clarification of the “Managed By” Test for Type B Investment Entities

Executive Summary

- Revenue Jersey has issued fully updated CRS Technical Guidance Notes (March 2026), replacing the 2017 joint CRS-IGA guidance. The document standardises industry practice and removes previous areas of interpretive flexibility.

- Jersey CRS Technical Guidance Notes (March 2026) https://www.gov.je/SiteCollectionDocuments/Tax%20and%20your%20money/Jersey%20CRS%20technical%20guidance%20March%202026.pdf

- The most material change for Jersey-regulated trust and company service providers (TCSPs / TCBs) is

- The strengthened and prescriptive wording on the CRS “managed by” test (Section VIII(A)(6)(b) of the Standard – pages 17–19 of the guidance).

- Key position (new wording):

- Where a regulated Jersey TCSP provides directors/officers and administers a Jersey company, the entity will be treated as being managed by a Financial Institution. This applies even where the directors act in an individual capacity, provided the contractual arrangement for director or management services sits with the regulated TCSP.

- Entities that also satisfy the gross income test (>50% of gross income attributable to Financial Assets on an aggregate 3-year look-back basis, or since inception) must now be classified as Investment Entities (Financial Institutions) rather than Passive NFEs.

- This shift triggers direct CRS due diligence, self-certification, reporting, and potential GIIN obligations on Equity/Debt Interests.

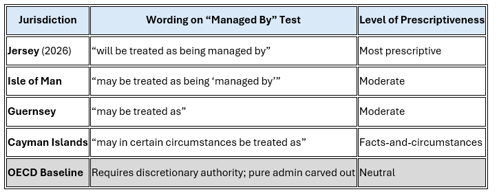

- While other Crown Dependencies use softer language (“may be treated as”),

- Jersey’s position is now the most prescriptive.

- The update is forward-looking only and does not affect any prior Revenue Jersey enforcement or remediation positions already communicated.

- Immediate action required:

- All Jersey TCSPs/TCBs should conduct a portfolio-wide classification review, update policies and training, and ensure robust documentation is in place.

- Background

- The March 2026 guidance consolidates and clarifies all key CRS compliance topics for Reporting Financial Institutions (RFIs) in Jersey.

- It reflects CRS 2.0 amendments (effective 1 January 2026) and provides clear, standardised expectations where multiple reasonable interpretations previously existed.

- The document explicitly states (paragraph 1.12–1.13) that its purpose is to “standardise application across the industry” and set “forward-looking expectations for RFIs”.

- Key Change – “Managed By” Test (Pages 17–19)

- Under the CRS, an entity qualifies as a Type B Investment Entity (and therefore a Financial Institution) if:

- Its gross income is primarily (>50%) attributable to investing, reinvesting or trading in Financial Assets AND

- It is managed by another Financial Institution (Depository Institution, Custodial Institution, Specified Insurance Company or Type A Investment Entity).

New Jersey position (extract from page 18):

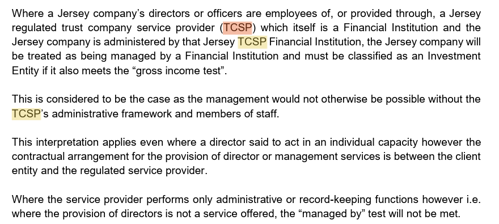

- “Where a Jersey company’s directors or officers are employees of, or provided through, a Jersey regulated trust company service provider (TCSP) which itself is a Financial Institution and the Jersey company is administered by that Jersey TCSP Financial Institution,

- The Jersey company will be treated as being managed by a Financial Institution and

- Must be classified as an Investment Entity if it also meets the ‘gross income test’.”

Important clarifications in the guidance:

- Applies even if directors are appointed in an individual capacity, provided the service contract is with the regulated TCSP.

- Pure administrative/record-keeping services (registered office, secretarial, bookkeeping, tax returns, financial statements) do not trigger the test.

- The test focuses on the existence of discretionary authority (implied or contractual) over Financial Assets under the TCSP’s governance framework.

- Three practical examples are provided (pages 18–19) to illustrate when the test is met versus not met.

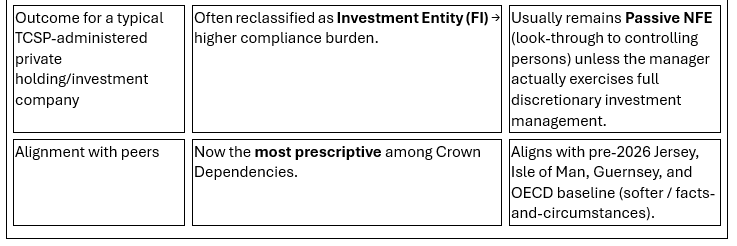

Impact:

- Many Jersey private holding/investment companies administered by regulated TCSPs that also provide directors will now clearly meet both tests and must be reclassified as Investment Entities (FIs).

3. Position in Other Jurisdictions

Jersey’s March 2026 update is now the clearest and most directive among the Crown Dependencies.

Looking further afield, Mauritius is not the same as Jersey following the March 2026 update.

- Jersey has taken a materially stricter and more prescriptive position than Mauritius (and most other IFCs) on the CRS “managed by” test for Type B Investment Entities.

Quick Comparison (as of 31 March 2026)

Bottom Line for Practitioners / Clients

- Jersey has deliberately removed previous flexibility. Many structures previously classified as Passive NFEs will now be treated as Investment Entities.

- Mauritius has not followed Jersey’s tightening. Its guidance remains unchanged in this area and continues to give TCSPs / management companies more room to argue that pure administration + director provision does not meet the “managed by” test.

If your clients are comparing Jersey vs Mauritius structures based on CRS compliance burden, Mauritius is currently more competitive / less burdensome for private wealth/family holding vehicles after the March 2026 change.

- Implications for Jersey TCSPs / TCBs

- Classification shift for many administered entities (from Passive NFE → Investment Entity FI).

- Upstream reporting impact – banks, custodians and other FIs will no longer look through to Controlling Persons; they will treat the entity as an FI.

- Client obligations – newly classified FIs may need GIIN registration (or sponsored/trustee-documented status) and must meet their own CRS responsibilities.

- Compliance burden – increased need for periodic reviews, updated self-certifications, and robust evidence files.

- No retrospective enforcement – the guidance explicitly protects prior Revenue Jersey positions already communicated to firms.

- Recommended Board Actions

- Portfolio Review – Immediately identify all administered Jersey entities where the firm provides directors/officers + administration services and reassess against both the “managed by” and gross income tests.

- Policy & Procedure Update – Revise internal CRS classification manuals and client onboarding/periodic review processes.

- Training – Deliver targeted training to all relevant staff on the new wording and evidence requirements.

- Documentation – Ensure every classification decision is supported by:

- Service/engagement letters showing the contracting party

- Scope of services (including discretionary authority)

- Governance/oversight arrangements

- Client Communication – Notify affected clients of any status change and assist with updated self-certifications.

- GIIN & Reporting Readiness – Confirm or obtain GIINs (or sponsored status) for newly classified FIs and integrate de-registration checks into entity wind-down procedures.

- Timing – Complete the initial portfolio review by 30 June 2026 (to align with the next reporting cycle) and embed annual (or 2–3 year) periodic classification reviews thereafter.

- Competitiveness Impact vs Other IFCs

- The update creates a marginal short-term competitive disadvantage for Jersey compared with other International Financial Centres (IFCs) in respect of private wealth / holding-company structures. Still, the overall long-term impact is expected to be neutral to positive.

- Why is it a potential disadvantage?

- Jersey’s prescriptive “will be treated as” wording will result in more entities being classified as Investment Entities (FIs) than under the softer “may be treated as” language still used in the Isle of Man and Guernsey.

- Consequence: Higher compliance costs (more periodic reviews, documentation, potential GIIN obligations, and entity-level reporting instead of look-through to Controlling Persons).

- Clients seeking minimal CRS burden may prefer IOM, Guernsey or Cayman structures for new private holding/family investment companies.

- Counter-balancing advantages - Certainty and risk reduction:

- The clear, standardised position reduces the risk of disputes with Revenue Jersey, enforcement action, or audit challenges.

- Institutional clients highly value this and align with Jersey’s reputation for robust, transparent regulation.

- Reputation premium:

- In a global environment of increasing OECD/EU scrutiny on “super-equivalence” and tax transparency, Jersey’s proactive standardisation strengthens its position as a leader in compliance.

- This can attract higher-quality, long-term business that prioritises regulatory certainty over marginal cost savings.

- No evidence of material client migration:

- The guidance is brand new (March 2026).

- Industry commentary and government reports to date do not flag this specific change as a competitiveness threat; instead, they emphasise Jersey’s commitment to meeting global standards while protecting its financial services sector.

- Net impact on Jersey’s competitiveness

- Private client / TCSP segment: Slight headwind for cost-sensitive structures.

- Institutional / funds segment: Minimal impact (funds are already typically FIs).

- Overall:

- Jersey continues to differentiate on quality, stability and compliance rather than regulatory flexibility.

- This aligns with Jersey Finance and government strategies that prioritise long-term reputation over short-term cost arbitrage.

- Sources

- Primary Jersey Documents • Full PDF – Jersey CRS Technical Guidance Notes (March 2026) https://www.gov.je/SiteCollectionDocuments/Tax%20and%20your%20money/Jersey%20CRS%20technical%20guidance%20March%202026.pdf

- Main Government AEOI / CRS Webpage https://www.gov.je/TaxesMoney/InternationalTaxAgreements/IGAs/pages/commonreportingstandard.aspx

- Supporting References • Taxation (Implementation) (International Tax Compliance) (Common Reporting Standard) (Jersey) Amendment Regulations 2025 (domestic law update) – available via the above AEOI webpage. • OECD CRS Consolidated Text (2025) and Commentaries https://www.oecd.org/ctp/exchange-of-tax-information/consolidated-text-of-the-common-reporting-standard-2025.pdf

- A time to win = https://www.gov.je/SiteCollectionDocuments/Government%20and%20administration/Time%20to%20Win%20report.pdf

- Mauritius Revenue Authority CRS Guidance Notes (latest, March 2026): https://www.mra.mu/download/CRSGuidanceNotes.pdf (see section 4.5.3 on Investment Entities and the “managed by” test)

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.